The latest GDP figures reveal that the RBA has got its wish of an economy growing so slowly that it teeters on the edge of a recession.

Now we wait to see if unemployment also starts to falter and tips us over that edge.

No, we are not in a recession, but cripes, the March quarter national accounts show an economy performing as badly as it can without actually being in recession.

The 0.1% growth in the March quarter is essentially a rounding error away from going backwards.

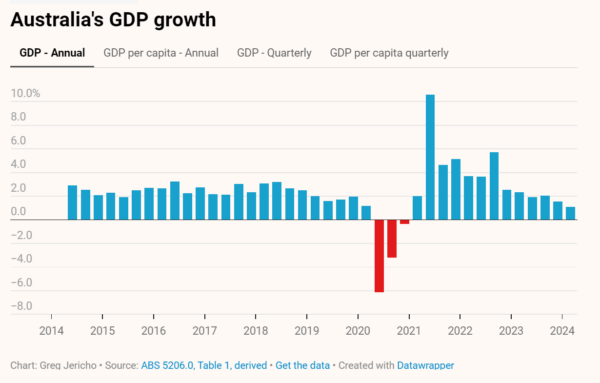

And things are no better if we look at annual growth. If we take out the pandemic period – when economic data really made no sense – the 1.1% annual growth of GDP is the slowest we have seen in Australia since March 1992.

Take out population growth and we have now had five consecutive quarters of the economy going backwards. It’s the first time that has happened since we started recording per capita growth back in 1973. That is not a record you want to be setting.

‘Sticky’ inflation is not falling – but it’s not rising, either. Why should that mean another RBA rate hike?

In the past year the economy shrank 1.3% when you exclude population growth. The pandemic years aside, that is the worst growth since December 1991, when we were in the deepest of deep recessions:

So no, not good.

Why are things so slow? Well, just take a peek at how much average interest repayments have gone up in the past two years:

The RBA has essentially done in two years what it took five years to do during the mining boom, when household incomes and wages were rising strongly. It has done this because the RBA believes that there is “excess demand” in the economy.

Clearly they have a different view of excess than the rest of us.

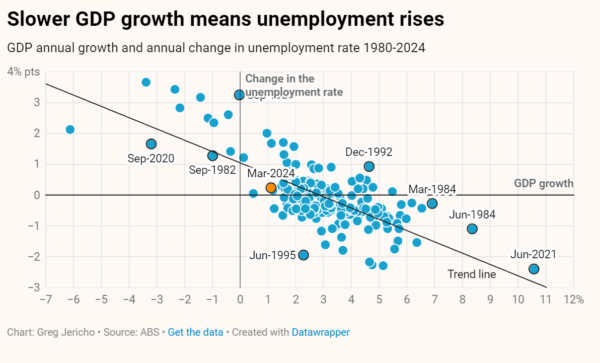

The only reason really to even care about GDP as a measure is that there is a generally solid link between it and unemployment. As a rule we need the economy to grow about 2.75% a year to keep unemployment stable. If GDP grows by less than that, unemployment usually starts rising:

If there was no link between GDP growth and unemployment, then to be honest it would be a meaningless number we might as well ignore.

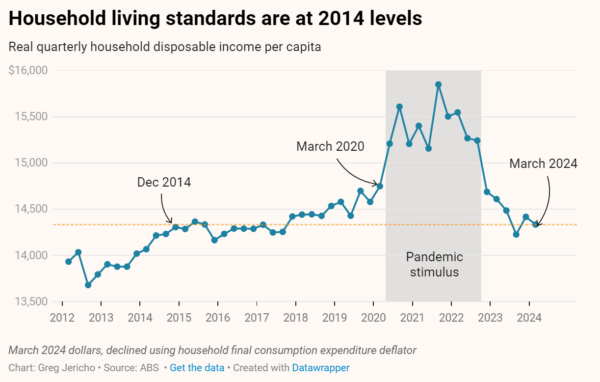

The other important thing about GDP is that households make up a bit over half of it, so if GDP is struggling there’s a good chance that people are, too – and right now the level of living standards of Australian households is back where it was a decade ago:

That is not a sign of health.

And what has been the big driver of weak living standards?

Well, did you remember my mentioning interest rate rises?

The increased cost of paying off home loans has had a major impact on people’s living standards, but so too has weak wages growth.

In the March quarter the average compensation for each employee rose 0.6% while the average cost of things we spend our money on (including bills) rose 1%.

Not surprisingly what we’re seeing is households spending very frugally. We never quite got back to spending as much as we likely would have were it not for the pandemic – but now the amount we’re spending is increasing by less than it was before 2020:

In the year to March, household spending rose 1.3% – around half the pre-pandemic rate. And any growth was mostly on essential items. Spending on essentials rose 2.1% over the past year, while spending on discretionary items – those things you buy when you are feeling good – rose just 0.1%.

That does not sound like excess demand to me, but apparently the RBA thinks it does.

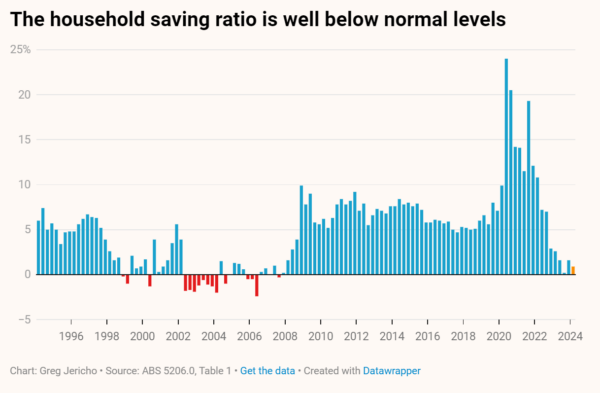

We aren’t spending more because we have so much more income, rather that we are saving less. The household saving rate was as low as it has been since 2008:

It means overall households did not contribute much to the growth of the economy, but to be honest, no one was really contributing to the growth of the economy because there was hardly any!

If you squint you could say the buildup of inventories is a sign that businesses hope to be able to sell stock later, but more likely it is just replenishing the stocks they have run down over the past few months rather than a sign of hope and optimism.

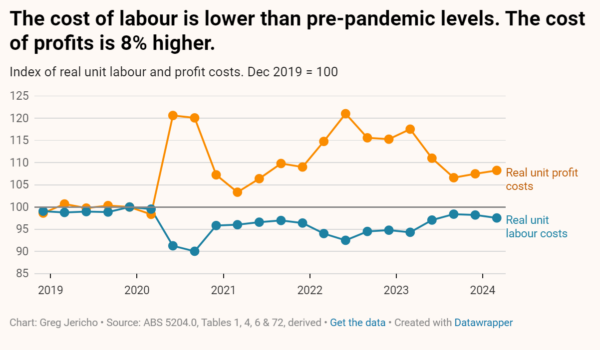

The cost of labour in real terms fell 0.7% in the March quarter to reinforce again that wages are not fueling inflation. The real cost of profits remains higher than it was before the pandemic, unlike labour costs:

The GDP figures show an economy that has been smashed by interest rate rises. The RBA believes we are too rich, too many of us are employed and we are spending too much money.

The GDP figures, however, show our living standards are as bad as they have been for a decade, our wages are not keeping up with our costs, and we are barely increasing our spending on anything other than essential goods and services.

Younger Australians feel like the game is rigged. And with the spending gap widening, who can blame them?

The economy has been going backwards for more than a year, except for population growth. Take that away and it looks like a recession. The only reason we are not in one is because – thankfully – unemployment has not risen sharply yet.

And let us hope that is not the next chapter of the RBA’s sorry tale of how the economy should be managed.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

The latest unemployment figures show the RBA has failed Australians

The Reserve Bank last week chose to keep interest rates high even as more people are losing their jobs.