Did business get their company tax cut after all?

The government tried to reduce company tax from 30 to 25 per cent but could not get that change through the Senate, except in the case of companies with a small turnover of less than $50 million. Since that defeat, the Business Council of Australia (BCA) has been arguing for cuts in company tax liabilities that might be delivered in other ways. Hence the BCA has argued for investment allowances. The head of the BCA, Jennifer Westacott, has made it clear that for the moment the BCA would be happy with a second prize when she said “An investment allowance is no substitute for a company tax cut. But if that tax cut is off the agenda for now, it doesn’t mean we can just stop thinking about how to boost investment. So, let’s take that first step to getting business investment back on track and introduce an investment allowance.” At the time Phil Coorey commented that a broad-based investment scheme would be a compromise.

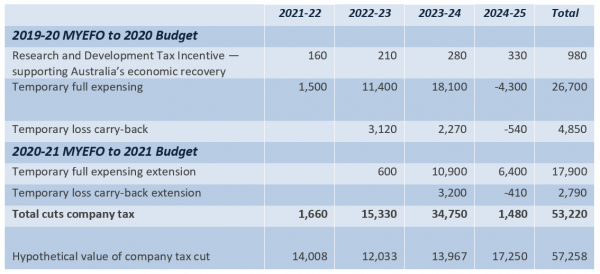

Since COVID, the government has announced various new tax concessions for companies which raises the question of whether the BCA got their compromise and how the funds involved compare with what a straight company tax cut would have delivered to business. Table 1 presents the various new concessions made for companies or businesses generally since the onset of COVID-19.

We include the three relevant measures covering the period from the 2019-20 Mid-year Economic and Fiscal Outlook (MYEFO) through to the 2020-21 budget and two further measures from the period from the 2020-21 MYEFO to the 2021-22 budget. Nothing of interest occurred in the intervening period leading up to the 2020-21 MYEFO. The value of all of those measures are given as their contribution to corporate income so that a measure that increases revenue is shown as a positive figure while a measure that reduces revenue is shown as a negative entry.

Table 1: New company tax concessions since COVID, $ million

We can see from Table 1 that the total value of the various tax cuts is very substantial, peaking at $34.75 billion in 2023-24. Over the forward estimates these measures sum to $53.22 billion. For comparison Table 1 includes an estimate of the value of the tax cuts had they been made as the government had planned. These are based on the actual value of company tax collected and correcting for the value of the concessional tax rate applying to smaller companies.

It is apparent that the measures summarised in Table 1 provided companies with almost all of what they would have received under the original plan of moving to a 25 per cent company tax rate. Indeed, if we added back the value of the tax cuts for smaller businesses then it is apparent that over the forward estimates, companies have received more than they would have under the original plan.

The benefits from this and last years budget are limited to those that invest in eligible capital assets and to those with turnovers less than $5 billion. The $5 billion turnover limit means that just 43 of Australian registered companies are excluded from this measure based on Tax Office data for 2018-19. Essentially there were two temporary measures introduced in the 2020-21 budget and extended in the 2021-22 budget. The full expensing measure allows the full cost of certain capital goods to be immediately expensed rather than being depreciated over time. The loss carry-back measure allows companies making a loss to apply that loss against taxed profits in previous years and receive a refundable tax offset. Given the temporary nature of these concessions it is most likely the BCA will push for further concessions in future years.