Housing affordability crisis – Saving for a deposit forever

The dream of saving for a deposit on a house is now so far beyond most poeple that even if you have a high paying job, you still can never save enough.

In 2015 former Treasurer Joe Hockey suggested to buy a house you just needed a “good job that pays good money”

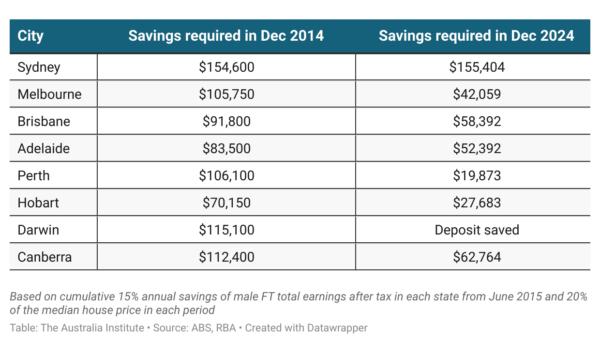

Ten years on new research shows that had a person on the average full-time male earnings in each state been saving 15% of their after-tax income, they would still be unable to afford a deposit on a median-priced house.

Worse than that, in Sydney they would have gone backwards. At the end of 2014 they would have needed a deposit of $154,600, but by the end of 2024 after saving $126,00 for 10 years they would still need an extra $155,404 in order to afford a 20% deposit on the median-priced house in Sydney.

As people have saved, the price of houses – and the size of the deposit needed – has kept going up, even faster.

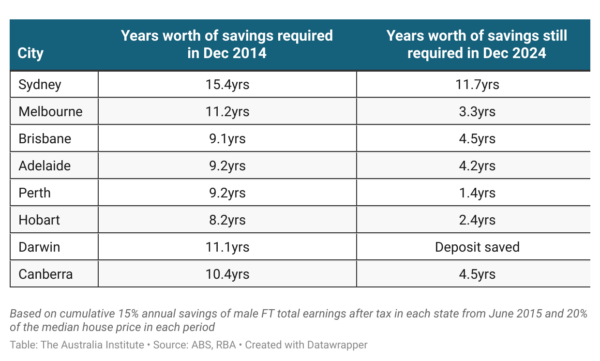

An alternative way to look at the issue is how many years left worth of savings do you still have to go after 10 years:

In Sydney the 10 years of saving has only wiped off 3.4 years of the 15.4 years you thought it would take to save for your deposit.

In Brisbane, what looked like needing just over 9 years to save, now 10 years later still needs another 4 and half years to go, but even worse as the above graph shows, savers in Brisbane have needed another 4 and half years for the past 4 and half years!

The reality is that for many people with “a good job that pays good money” the possibility of owning a home is out of reach without help either from a partner who also has a good job or the bank of Mum and Dad (who would also have needed that good job).

25 years of the tax system incentivizing housing speculation through the 50% capital gains discount combined with negative gearing has left Australia with a housing affordability crisis.

The 50% discount and negative gearing now cost around $12bn a year with $7.2bn going to the richest 10%.

The upcoming election needs to have housing affordability front and centre. After 25 years we need to stop doing what isn’t working and start fixing things.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

It’s impossible to be single and save for a deposit in Sydney – no matter how good your job is

For most people in Sydney – if you had started saving for a house a decade ago, you would be further away from your goal.

Crushing the Australian (and Elinor’s) dream

A number of the housing policy proposals on offer in this election will make affordability worse.

Housing affordability to get worse as big corporates do annual tax magic

Renting a place to live is getting more expensive and house price rises are tipped to accelerate.