More evidence that inflation is under control – but where is the RBA?

Inflation is under control and the economy is barely staying out of recession. But the Reserve Bank has decided to take more than 2 months off before deciding if a rate cut is needed.

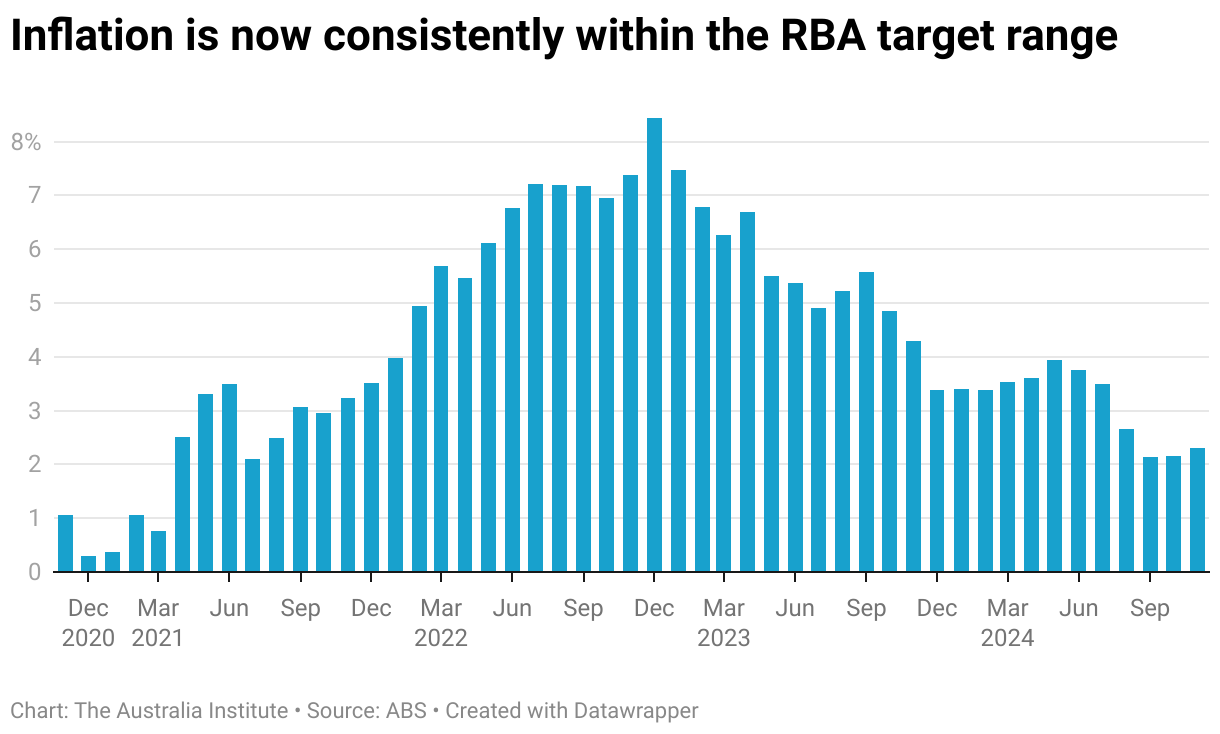

The November Consumer Price Index inflation figures out today showed that inflation in the past year rose 2.3%, marginally up from 2.1% in October. The combination of efforts by the government to limit energy costs and the continual easing of inflationary pressures across the world means that inflation is now firmly within the Reserve Bank’s target range of 2% to 3%. And yet the Reserve Bank board is still on holidays for another 6 weeks – meaning Australians will have to wait longer than they should for any relief from a rate cut.

The November CPI figures highlight that inflation is no longer the great concern it was 18 months ago. Even with a 22.4% increase in electricity prices due to the “the return to a single monthly instalment of the 2024-25 Commonwealth Energy Bill Relief Fund rebate for households in South Australia, Tasmania, Northern Territory and ACT, and for most households in New South Wales and Victoria” the overall inflation growth of 2.3% remains in the bottom half of the RBA’s target.

Even more clear is that despite the slight increase in the CPI, the Reserve Bank’s “trimmed mean” measure of underlying inflation fell from 3.5% to 3.2%.

Inflation is not rising in a manner consistent with the need for high interest rates. Wages growth has peaked and price growth similarly continues to slow.

Now is the time for the Reserve Bank to cut interest rates, and yet the RBA board does not meet until the 17th and 18th of February. At that point they will have not met for over two months since the last meeting on the 9th and 10th of December. There is no justification for having such a large break.

Last year saw the introduction of board meetings every 6 weeks, which should mean that there is a meeting on the 20th and 21st of this month. In the past the RBA board routinely did not meet in January given meetings were previously held on the first Tuesday of each month, but there is no reason why the first meeting of the year could not have been 6 weeks from the last meeting in December, or at the very least in the first week of February.

A meeting in the first week of February would at least allow the board to consider the December quarter CPI figures, which are released on 29 January. That is the last release of major data needed for the RBA to make its decision – given the next wage price index figures are released on the day after the RBA board meets!

Since the middle of 2022, around half of the increase in cost of living for households has been due to rising mortgage repayments. That cost has led to a slowing Australian economy which is currently staying out of a recession only due to government spending and population growth. There is no heat in the economy, no demand pressures that need to be restrained.

It is well past time for the RBA to cut rates, and they should be doing so much earlier than in 6 weeks time.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.