Sorry, Coles and Woolworths, but high wheat prices are not to blame for your bread prices

At worst at worst, the increase in wheat prices should have caused a 0.75% increase in the price of bread. Instead they soared.

The focus on the ability of the two major supermarkets, Coles and Woolworths to charge high prices due to a lack of competition and the cover of higher overall inflation has placed a very bright spotlight on the operations of the two retail giants.

Woolworths has responded to the criticism of their (former) CEO’s appearance on ABC’s 4 Corners by amazingly finding the ability to lower prices! Woolworths has announced that it “has dropped the price of more than 400 items by an average of 18% to help customers spend less when they shop at the supermarket this Autumn”. This is quite an extraordinary move by a company that said it was already running on thin margins and constrained by rising costs. It would seem that it does actually have the ability to lower (and raise) prices at its discretion rather than being hostage to demand and supply.

Coles CEO Leah Weckert however has defended Coles pricing by blaming rising costs – especially wheat.

She is reported stating in an AAP story that “food inflation had been significantly lower in Australia than other developed economies, and a lot of it had to do with higher import prices, partly due to the war in Ukraine and its impact on wheat prices.”

Businesses are quick to blame the costs of inputs for their price rises. However an analysis of the “input-output” tables of the national accounts reveals that these claims do not hold up.

The latest data we have on the total inputs and output in the Australian economy is from 2020-21. In that year the sheep, grains beef and dairy cattle industry contributed output worth $71 million directly to bakery product-manfuactuing. It is fair to assume all of this is from grain.

There was also another $843 million contributed by the industry “Grain mill and cereal product manufacturing”. We are then able to calculate that the “sheep, grains etc” industry contributed 31% of the final value of the “grain mill etc” industry.

That means the indirect contribution of grains to bakery product manufacturing was $259 million plus the $71 million from sheep, grains beef and dairy cattle industry for a total grain input of $330 million.

Total bakery production was $8,559 million of which $6,968 million was purchased by consumers. But the final price to consumers included wholesale services worth $429 million and retail services of $3,768 million bringing the total final consumer sales to $11,165 million.

This means that out of the total sales to consumers worth $11,165 million, the cost of the grain input was $330 million multiplied by the share of output that is purchased by consumers which was $269 million or 2.4%. So this means that the price of wheat only makes up 2.4% of the cost of a loaf of bread you buy in the shops.

On those figures, a doubling of the grain prices would warrant a price increase for bread of just 2.4%. Federal Government figures show that milling wheat prices rose from about $480/tonne in February 2022 to peak at about $630/tonne in June that year and have since fallen back to $440/tonne, less than just prior to the invasion of Ukraine. At worst then, there was a 31% increase in grain prices from before the invasion to the peak. That would have accounted for, at worst, a 0.75% increase in the price to Australian consumers but that should have disappeared by now.

So what happened to bread prices?

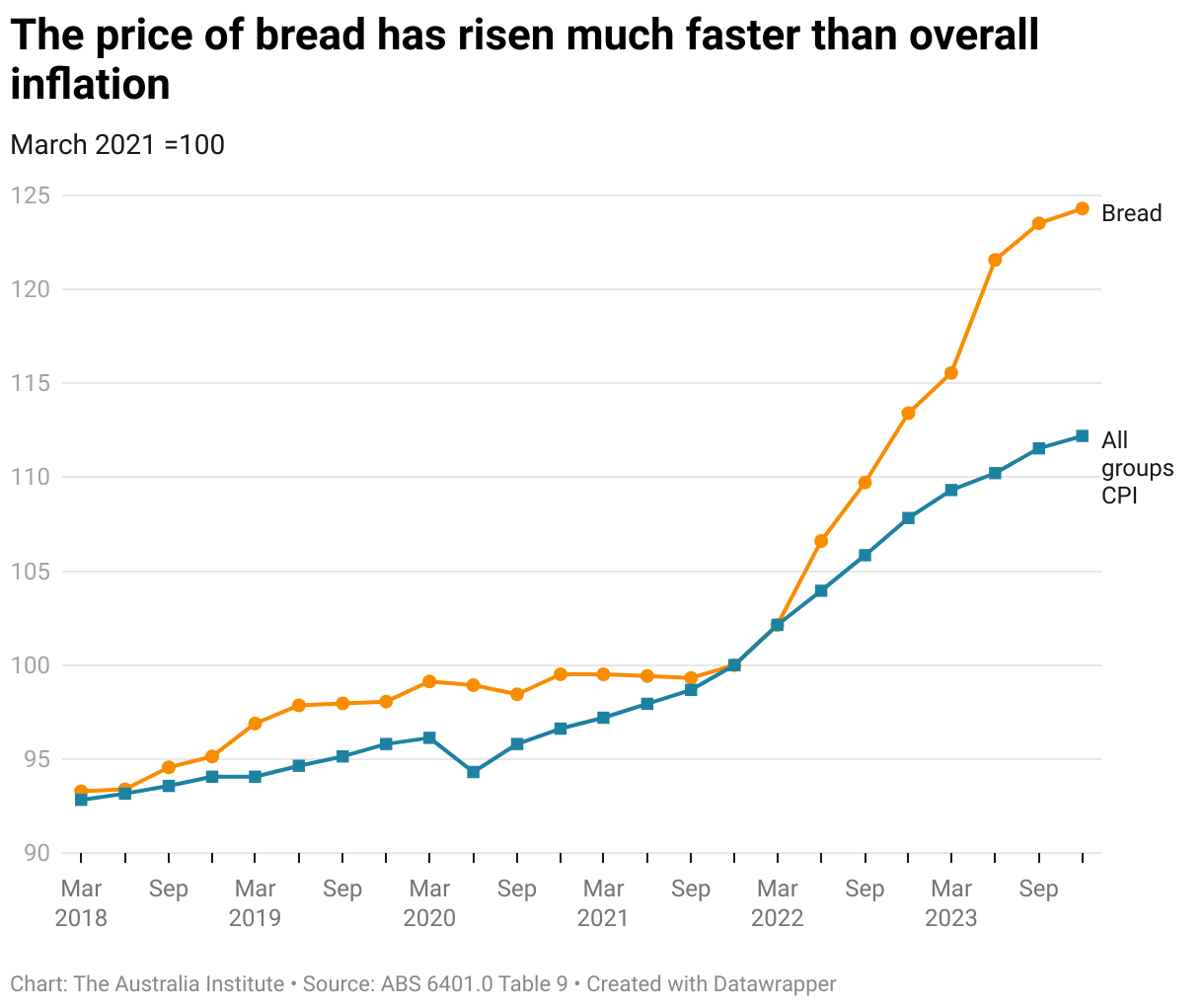

All-groups CPI increased by 12.2% since March 2021 while bread prices increased by double that amount at 24.3%. Quite clearly it is unfair to put the blame on grain prices.

The reason bread prices and those of other grocery prices is rarely as linked to the cost of agricultural products. Supermarkets have the power to set prices, and they do so in order to make the most profit, not to just cover costs, and when costs do increase that gives them a great opportunity to justify their fattening their profit margins.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Coles guilty of fake discounts, but it shouldn’t be the only corporate giant taken ‘down, down’ for gouging Australians

The Australia Institute welcomes the Federal Court’s finding that Coles has misled Australian shoppers by promoting fake discounts on everyday grocery products.

In Trump we trust? | Between the Lines

The Wrap with Bill Browne Prime Minister Anthony Albanese returns from a meeting with the mercurial US President Donald Trump, a great diplomatic success by the usual measures. Trump said without hedging that Australia would get nuclear-powered submarines under the AUKUS pact and inked a critical minerals deal to “unlock” private investment. The media lapped

Why the wealthiest don’t need another tax cut

Australia is a low taxing nation, but Shadow Treasurer Tim Wilson still seems to want the highest earners to pay less.