The latest inflation figures released on Wednesday showed that inflation is “sticky” and is no longer falling at the pace it was earlier this year.

But while there will be those arguing this means we need higher interest rates, the latest retail spending figures – also released this week – show that’s the last thing the economy needs.

There is often a curious bit of fudging around how inflation gets talked about. We sometimes hear the RBA and others worry about “accelerating” inflation, that is, when the growth of prices (inflation) is itself speeding up.

Prices as a rule always go up, but what economists suggest they care about is when the amount by which they go up “accelerates”. We see this when the annual inflation figures rise as they did in 2022 and 2023.

Over the past year or so prices have still been rising, but the rate of inflation has been falling, or “decelerating”.

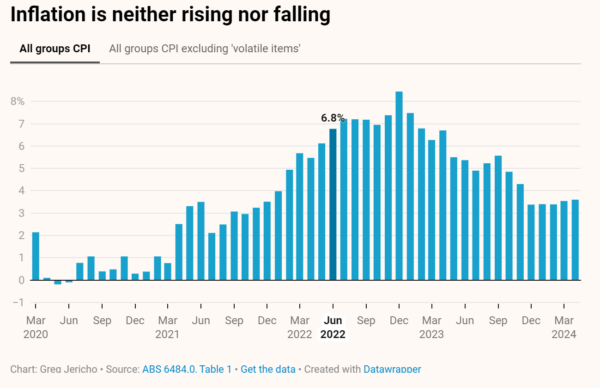

But, in the past four months, inflation growth hasn’t been accelerating or decelerating. It has been stuck at about 3.5% to 3.6%. This is why you’ll have heard some commentators talk about “sticky” inflation:

In the year to April, inflation rose 3.6% up from 3.5% on March. But the monthly inflation figures can be a bit erratic, so we can also use the measure that excludes “volatile items”. On this measure, inflation remained steady at 3.5%.

On both measures, however, prices are still rising by more than the RBA’s target ceiling of 3%.

And this is where the fudging occurs. Suddenly it is clear some economists don’t actually care so much about “accelerating” inflation – they just care about inflation being above 3%.

Sign up for Guardian Australia’s free morning and afternoon email newsletters for your daily news roundup

It is worth remembering that the 2% to 3% target range is not an immutable economic law of nature; it’s just an arbitrary goal. The RBA’s actual “duty” is to “contribute to the stability of the currency” – which is precisely what we have right now.

Yes, inflation is “sticky”, but sticky doesn’t just mean not falling, it also means not rising.

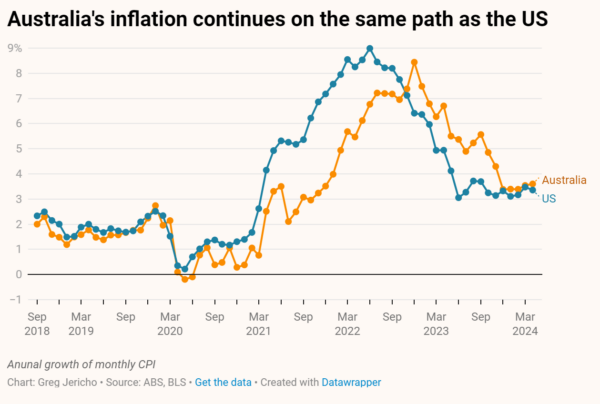

And we are not alone in dealing with this.

In the past I have noted that Australia’s inflation has essentially gone up and down in line with the United States and, completely unsurprisingly, it has also followed the US in being “sticky”:

So does sticky inflation mean we need to hit households again with higher interest rates? Do you really think our economy will be so much better if inflation was “sticky” at, say, 2.9% and thus within the RBA’s target band, instead of where it is now at 3.6%?

Is that benefit worth sending 80,000 or so people out of work?

I don’t think so.

We need to also remember that when we talk about inflation we are talking about the consumer price index. The key aspect is consumers.

Are consumers out there acting in a way that would suggest they are the ones driving up prices through strong spending? Not at all.

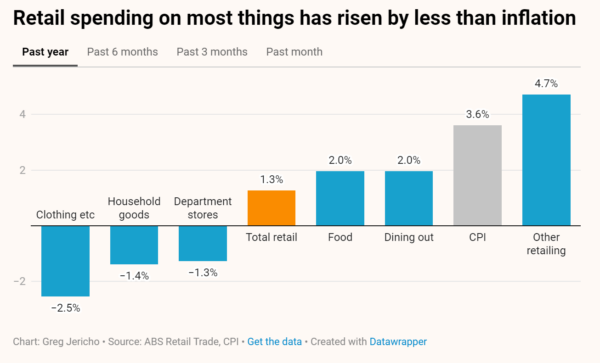

The latest retail trade figures out on Tuesday showed that annual spending in shops rose just 1.3% in the year to April. Given inflation rose to 3.6%, that means we actually bought a lesser volume of things in April this year than we did a year ago:

It’s also worth noting how weak that 1.3% growth is. Over the past 30 years the average annual growth of retail spending has been about 4.8%:

In the years before the pandemic, Australia’s economy was pretty anaemic. Spending was down and there was little demand in the economy, and yet by comparison that looks like a golden period compared with now.

That 4.8% average growth includes the increase in prices. So given inflation is higher now than it has been in the past, you would expect the amount of money we are spending in the shops is naturally higher because the cost of things is rising faster. But no.

We also see this lack of spending when we look at the actual volume of retail spending.

During the pandemic, there were a lot of falls and spikes in how much we bought because of the lockdowns. In early 2020 we bought a lot of stuff. But since then we have bought less and less.

This was expected, but the amount we spent didn’t just fall back to the long-term trend level; it has fallen well past that:

In the first three months of this year we bought about 2% less stuff from shops than the long-term trend – that’s about $2.4bn less.

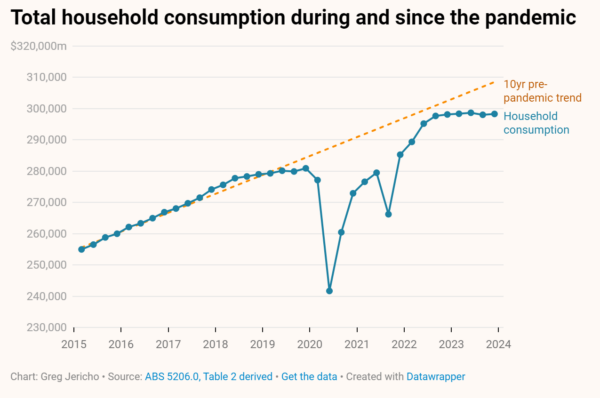

This also aligns with our total consumption – which includes other things beside retail, such as petrol, rent, insurance and medical bills.

Our total consumption never recovered fully from the pandemic to be back at the level that would have been expected:

Does this suggest households going out spending wildly and needing another rate rise to teach them a lesson?

Compare this with the mining boom years – a period in which it was obvious to all that the economy was running hot with strong wage growth and increased spending (and ever more tax cuts and handouts from the Howard government):

Now that was a case of excess demand.

What we are seeing now is not consumers spending either more than expected or in a manner that would drive up prices. The retail figures show that households are largely reducing the amount of things they are buying and adjusting their purchases to cheaper items.

Inflation might be sticky, but it is not the fault of consumers. And another rate rise would be just punishing Australians for something they had no role in causing.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.