Australians are hurting from rate rises more than anyone. But that doesn’t mean the Reserve Bank is about to start cutting.

This week the IMF told Australians what we already knew – we are hurting from rate rises more than anyone. But that is unlikely to mean the Reserve Bank is about to cut rates.

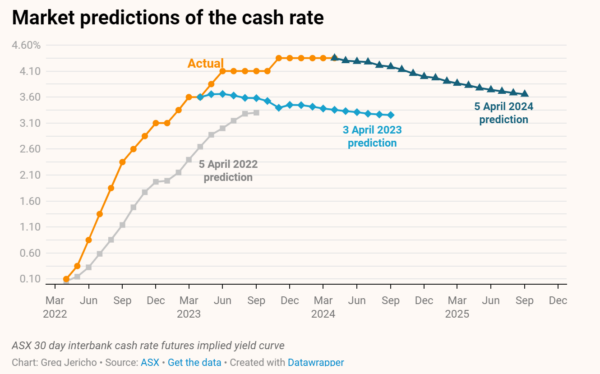

The market expectation is that by this time next year the RBA will have cut rates twice to 3.85%. If that is comforting, just remember that a year ago the market predicted the cash rate would now be 3.35%, not 4.35%. It was only out by a full 100 basis points.

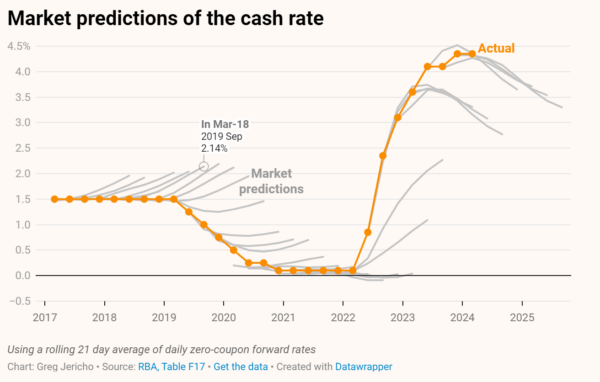

Investors are not great at predicting where the cash rate will be in a year’s time.

Through 2017 to 2019, investors were sure the RBA was about to raise rates. It didn’t. When the RBA began raising rates in 2022, investors underestimated how quickly and by how much the bank would increase them. Through 2022 and the start of 2023 investors (and I must admit myself) assumed we must have reached the peak and yet the RBA kept going that bit higher.

The good news for those struggling with a mortgage is that since the middle of last year investors have mostly got it right and so the chance of a rate cut before another rate rise does seem more likely than not.

But if you are struggling, do not feel that you are alone, because the IMF this week estimated that Australians feel the pinch of rising interest rates more than those in any other advanced economy.

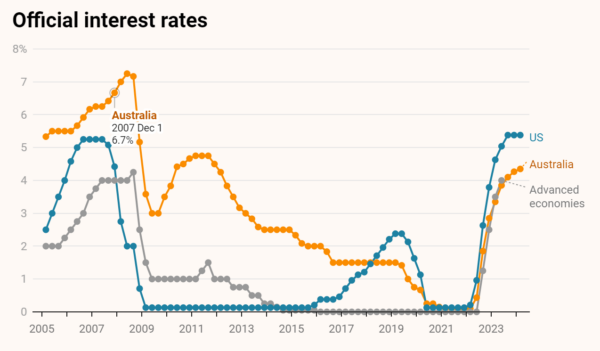

Since the pandemic the RBA has increased interest rates largely in line with other advanced economies, if a little bit behind the US:

But rates going up at the same rate does not mean they have the same impact on households.

The reason the IMF argued Australians are affected more by rate rises than others came down to five issues.

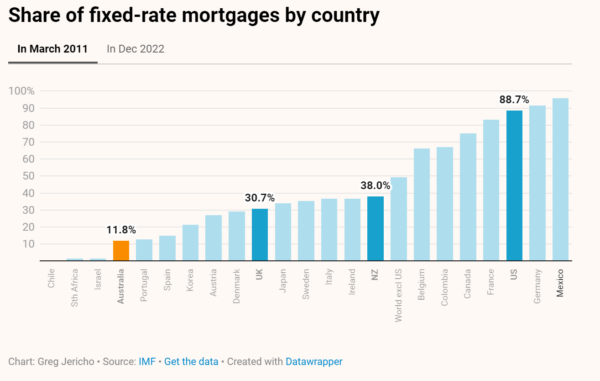

The first is our variable mortgage rates.

Even though we have become slightly more amenable to taking out fixed-rate mortgages we still greatly prefer variable rate unlike in most other advanced economies. Almost all mortgages in the US are fixed rate as are 86% in the UK, compared with just 15% here:

That means interest rate rises here hurt almost all mortgage holders, whereas in the other nations they mostly affect prospective buyers.

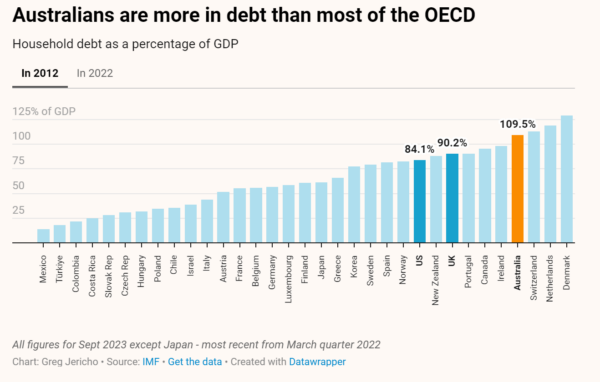

The second issue is how much debt we hold.

More debt magnifies the impact of rate rises on that debt. And, boy, do we like debt. Among the OECD only Swiss households hold more debt than Australians:

The third reason for Australia’s greater sensitivity to rate rises is how leveraged we are and supply constraints. Australia has looser loan-to-value limits which make it easier for homeowners here to use their houses as collateral against additional borrowing.

The fourth reason is that our housing supply constraints are worse than most nations.

One area the IMF is silent on is the fifth issue of house prices. It makes no comment on whether Australian houses are more or less overvalued than in other nations.

But the IMF does provide an index of median house prices across advanced economies. When we compare that with Australian house prices, it’s clear house prices here are rising much faster than elsewhere:

Since 2005 Australian average house prices have risen 160% compared with the 86% rise across advanced economies. Since the start of the pandemic house prices in Australia have increased more than double the pace of prices in other advanced nations.

Our debt, love of variable mortgages and high house prices altogether means Australians feel rate rises more than any other advanced economy.

This, however, does not mean the RBA will cut rates sooner. It may very well worry that we will feel the benefits of rate cuts more than in other nations.

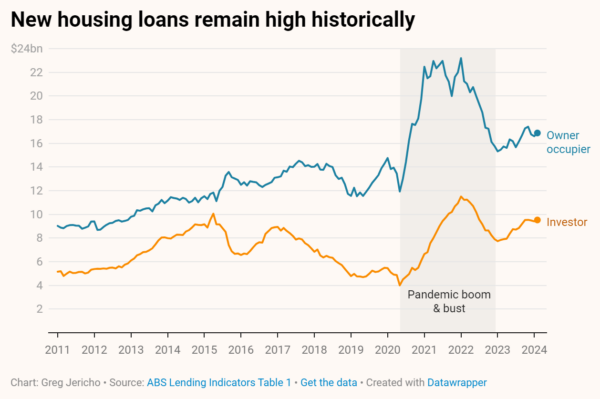

The latest lending figures out this week also do not suggest rates will be cut. New mortgages over the past year were up 13% and driven as much by investors as owner-occupiers:

While there was a big drop in lending after the pandemic boom, the actual value of new loans remains higher than would have been expected before the pandemic. The RBA will be likely hesitant to cut rates while we’re still borrowing more than we ever have:

But thankfully any further rate rises seem unlikely.

The wage rise data for enterprise bargaining agreements out this week suggest the peak of wage growth as with inflation is also behind us. This highlights yet again that there is no wage-price inflation and no need to try to smash income growth:

With no reason to raise rates further but a tendency to worry that cutting rates may set fire again to house prices, calls that a rate cut is coming soon may unfortunately be optimistic. And rather than acting, the RBA may decide that doing nothing is a safer option than either raising or cutting rates.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?