Tax cuts like shooting yourself in the foot: new data shows

Instead of reloading the gun to do it again, perhaps this is a good time to reconsider whether company tax cuts made any sense at all

The Australia InstituteFollowJan 25

The Australia InstituteFollowJan 25

The ABS released its detailed biennial survey of employment arrangements this week and, buried deep in the dozens of statistical tables, there was a very surprising breakdown.

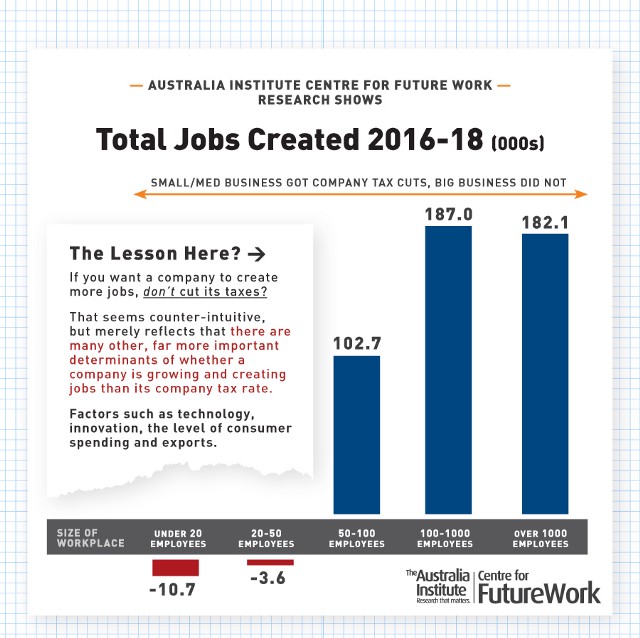

It turns out that Australia’s biggest workplaces (both private firms and public-sector agencies) have been the leaders of job-creation over the last two years.

This runs against the common refrain that small business is the “engine of growth.”

In fact, workplaces with less than 50 employees actually shed employees (14,000 in total) since 2016. But curiously, it was only smaller businesses that received the much-vaunted reduction in company tax (from 30 to 27.5 per cent), beginning in 2016.

The tax rate for small and medium-sized businesses began to fall in 2016, first for the smallest firms (with turnover under $2 million), and then for firms with up to $50 million revenue.

The tax is based on turnover, not the number of employees; nevertheless, the vast majority of firms which have received a tax cut have less than 50 employees. Yet that is the group that has reduced its workforce since company tax cuts began to be phased in.

In contrast, very large workplaces (with over 1000 employees) added 182,000 new jobs over the two years. Workplaces with between 100 and 1000 employees added 187,000. But very few of those workplaces would have received the reduction in company taxes (since most would exceed the $50 million annual revenue threshold).

Workplaces between 50 and 100 employees created a net total of 103,000 new jobs between 2016 and 2018. Some of those firms would have received the tax cut, and some not — depending on the nature of the business and the amount of total turnover generated per employee.*

The share of small businesses (under 50 employees) in total employment declined by two percentage points — since they were reducing their workforces, while larger companies were growing. Small businesses (under 50 employees) now account for 34 per cent of all employees, compared to 36 percent in 2016.

So, why would large companies that didn’t get a tax cut create new jobs faster than companies which did benefit from the Coalition tax cuts?

Simple: there are dozens of different factors which determine whether a company is profitable or not, and whether it chooses to grow. Tax rates are just one of those variables. Others include:

- Growth in consumer demand.

- The company’s investments in product quality, innovation, and design.

- Production costs.

- Interest rates and financing costs.

- Business confidence and expectations.

- Management capacity.

- International competition.

Trends in all these other factors can easily overwhelm the marginal impact of lower tax rates. Small business sales, in particular, have been held back by stagnant wages among Australian workers.

Even companies which experience higher profits due to lower tax rates may choose to simply accumulate those profits, or pay them out to shareholders in dividends and share buy-backs (instead of expanding payrolls). Empirical evidence shows this has been the dominant impact of U.S. business tax cuts implemented by Donald Trump.

Changes in tax rates can even have offsetting effects which undermine business conditions and hence reduce job-creation: if the revenue lost to tax cuts results in corresponding reductions in government program spending or infrastructure investments (as seems likely), then overall business conditions might be weakened, not strengthened.

The reduction in employment by the businesses which most benefited from the expensive business tax cuts over the past two years, should lead policy-makers of all persuasions to reconsider the argument that this is an effective way to stimulate growth and job creation. However, in October the government announced it wanted to accelerate the next stages of the small business tax cuts — taking the rate down to 25 per cent five years faster than originally planned.

So far, the policy is akin to shooting oneself in the foot. Instead of reloading the gun to do it again even sooner, perhaps this is a good time to reconsider whether the strategy makes any sense at all.

From all of the team at The Australia Institute, thanks for reading.

We are able to do what we do because of your support.

Subscribe to our mailing list to receive updates like this, straight to your inbox.

*Data on job-creation by firm size is detailed on Table 13 of Data Cube 1, in the “Downloads” section of this ABS report. The data refers to waged employees, not including owner-managers of businesses.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

The stark reality we need to face about guns in Australia

The horrific anti-Semitic terrorist attack in Bondi, the most deadly mass shooting since the Port Arthur massacre thirty years ago, makes gun law reform in Australia necessary. Suggestions from former prime minister John Howard and others that gun law reform is just “a distraction” are cynical in the extreme. Precisely no one is suggesting gun

Gun law fail: Dodgy licences lead to firearms flood

Hundreds of thousands of gun owners have no genuine reason to have a firearm according to analysis released today by The Australia Institute.

What’s the point of a gas exports tax?

On this episode of What’s the Point?, Richard Denniss discusses how global gas industry has pulled off the greatest con in Australia’s history, and why Australians are living with the consequences. He spells out the simple steps we need to take to fix it. This episode was recorded on Friday 10 July. Host: Richard Denniss,