The fiscal cliff has arrived

The Australian carried the headline “Super spending event”, which seems to reflect a lot of the press coverage which has treated the 2021-22 budget as a big spending budget.

The government is keen to convey the impression that this budget will contribute to the momentum of the recent economic recovery. That contrasts with the discussion earlier this year (2021) when there were many expressions of concern about the looming fiscal cliff. The “fiscal cliff” referred to the huge reduction in stimulus spending associated with the end of the JobKeeper program and the coronavirus supplement to JobSeeker. (See here and here)

So, is there a fiscal cliff? Data reported by the Parliamentary Budget Office shows that government outlays were substantially higher in the June and September 2020 quarters but then fell substantially in the December quarter and by the March 2021 quarter were not much higher than the March 2020 quarter before the COVID stimulus kicked in.

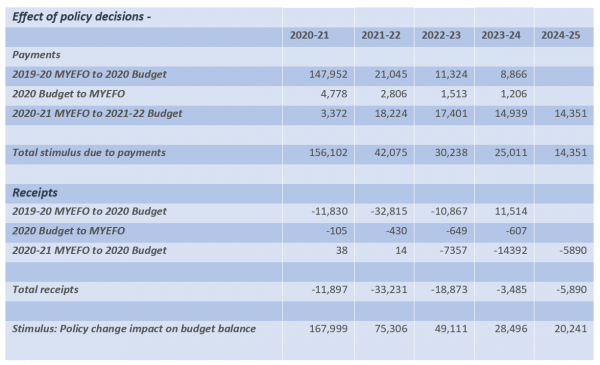

We are now able to present data for the stimulus since the onset of COVID based on all the initiatives to date. Each year the budget announces estimates of the budget magnitudes for the budget year and the three subsequent years. But of course, in each budget the new magnitude forecasts are different from the forward estimates because of two classes of events:

- First the government makes a number of changes to tax rates, payments it intends to make and so on. These are referred to as “policy decisions”.

- Second there are changes to expected receipts and outlays as a result of unforeseen changes such as higher iron ore prices increasing tax receipts, higher unemployment increasing JobSeeker payments and so on. These are referred to as “parameter and other variations”.

Fortunately for researchers, the budget papers give a breakdown of future changes in the budget position as a result of policy changes as distinct from changes due to changes in underlying social and economic conditions. (See Table 3.5 here.)

Table 1 is constructed so as to gauge the degree of stimulus the government has delivered since the beginning of COVID-19 and how that is changing over the forward estimates.

In March 2020, the government started to make announcements on JobKeeper and the JobSeeker supplement. We include the new policy initiatives outlined in each of the 2020-21 and 2021-22 budgets as well as the 2020-21 MYEFO. Those are given separately for payments (e.g., Jobkeeper, Jobseeker etc.) and receipts (e.g., tax concessions for business and individuals etc). For example, in the 2019-20 budget there were new payments of $147,952 million and tax cuts of $11,830 million which applied to the 2020-21 year. Following that budget, some additional announcements were made in the MYEFO which added $4,778 million to payments and reduced tax by $105 million. Finally, the 2021-22 budget added a further $3,372 million to payments and added $38 million to tax.

All of that added up to a cumulative stimulus of $167,999 million shown in the final row for 2020-21 as shown in the bottom row of Table 1.

Table 1 show that the stimulus in 2020-21 was a substantial $167,999 million but that falls by almost one hundred billion to $75,306 million in 2021-22, with additional falls in the following years.

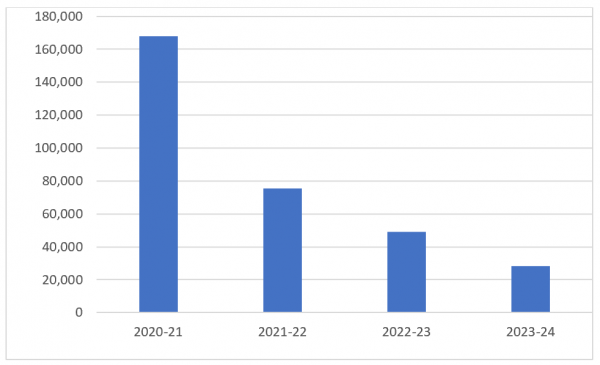

The total stimulus as given in Table 1 is depicted in Figure 1 for 2020-21 and the forward estimates.

Figure 1 clearly shows the extent to which the stimulus is going to be withdrawn over this and subsequent years. This is indeed the “fiscal cliff” some commentators have talked about.

The government would have felt encouraged by the strength of the economy despite the reduction in stimulus since the September quarter peak. Employment has continued to increase and unemployment was allowed to fall. As the stimulus from 2020-21 wears off we should expect to see the economy return to something like the conditions we experienced prior to COVID. We would expect the withdrawal of the stimulus to be associated with a weakening of the economy in the near future.