The fiscal cliff

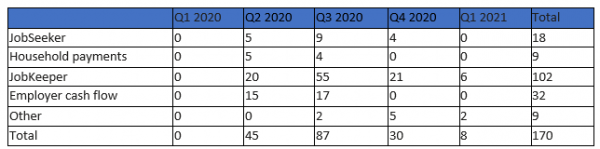

The stimulus value of the Budget is clearly a relative thing. The stimulus due to JobSeeker and JobKeeper is due to end in December 2020 and March 2021 respectively. Based on some data supplied by UBS we can illustrate the size of the Government’s fiscal stimulus since the outbreak of COVID-19. Those figures are shown in Table 1 on a quarterly basis.

It can be appreciated from Table 1 that the stimulus as measured by the items identified here peaked at $87 billion per quarter in the third quarter (the September quarter just gone as this is being written). For that quarter alone the stimulus was 17 per cent of GDP. These are very large figures in terms of the degree of fiscal stimulus involved. But having a massive stimulus supporting the economy means there is going to be a massive contractionary effect when that stimulus is withdrawn.

The Government says that it is maintaining a stimulus to support jobs, but we can determine the value of that stimulus compared with the stimulus about to be withdrawn.

From the budget papers we can examine the new policy proposals and figure out their contribution to the stimulus for each of the forward estimate years (2020-21 to 2023-24). Table 2 shows the effect of policy decisions insofar as they change the budget magnitudes.

Table 2 shows that the stimulus value of the measures in the 2020-21 Budget are worth $139.6 billion in 2020-21 or 7.2 per cent of GDP. Recall that the stimulus for September 2020 alone is worth 17 per cent of GDP. In 2021-20 the stimulus then falls to a low 2.6 per cent of GDP, 1.0 in 2022-23 and virtually down to nothing in 2023-24.

In the face of the looming fiscal cliff we wonder about the forecast employment growth at 2.75 per cent in the present year and then 1.75 per cent in 2021-22, and then one per cent and 1.75 per cent in the subsequent years.

This is a concern. Over the forward estimates based on Statement No 1 in Budget Paper No 1, economic growth will be 9.2 per cent but employment growth will be close to that at 7.4 per cent given the above figures. The concern is that these figures suggest very low productivity growth of 0.4 per cent per annum coming out of the slump. Moreover, the assumed economic growth is problematic in the context of a massive withdrawal of the economic stimulus. We suggest the Government’s employment forecasts are optimistic and the assumption that the growth will be experienced mainly as employment growth – and not as productivity growth – is perhaps unrealistic.