The rate rises have cost households and businesses billions of dollars

The rate rises over the past 2 years have seen banks taken billion from households and business in increased interest payments.

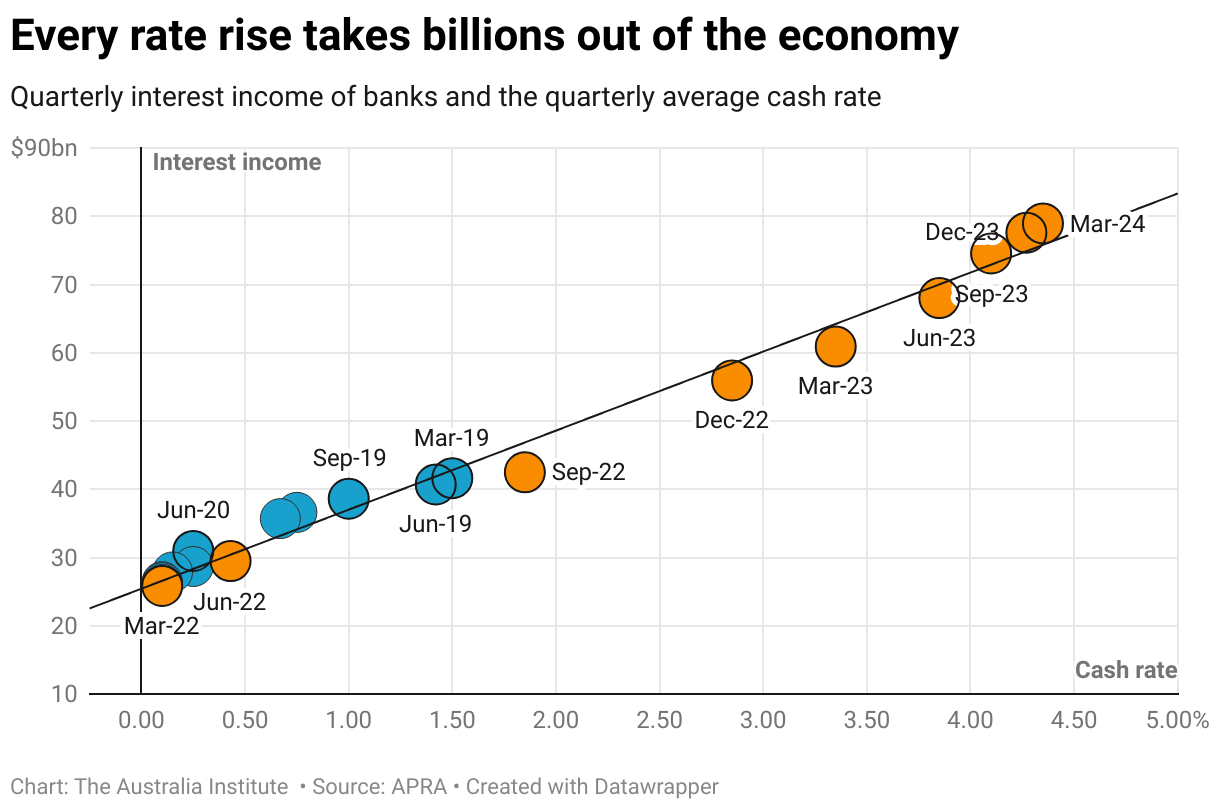

New APRA figures show the impact the Reserve Bank’s program of official interest rate increases has had on the Australian economy.

From the low of 0.10% in April 2022, official interest rates have increased by 425 basis points to 4.35%. Thankfully the Reserve Bank has this month kept rates steady, but the damage to the economy has already been done.

Since the March quarter of 2022, quarterly interest payments to the banks from the rest of the Australian economy went from $25.8 billion to $78.95 billion in March 2024. If we annualise these figures that means there has been a $212 billion increase in payments to the banks since official rates were increased.

Since that low of March 2022, each 25 basis point increase in the official interest rate increased banks’ annualised interest charges by around $12 billion. For comparison that is slightly more than the Australian government is budgeted to spend in this financial year on support for carers.

Over the same period, quarterly payments to the banks for home loans increased from $13.5 billion to $32.8 billion. The increase of $19.3 billion per quarter equates to just over $77 billion per annum. It also means that each 25 basis point increase in the official rate increases annualised interest charges on home loans by $4.5 billion per annum. Each 100-basis point increase increased the banks’ annualised interest charges on home loans by $18 billion.

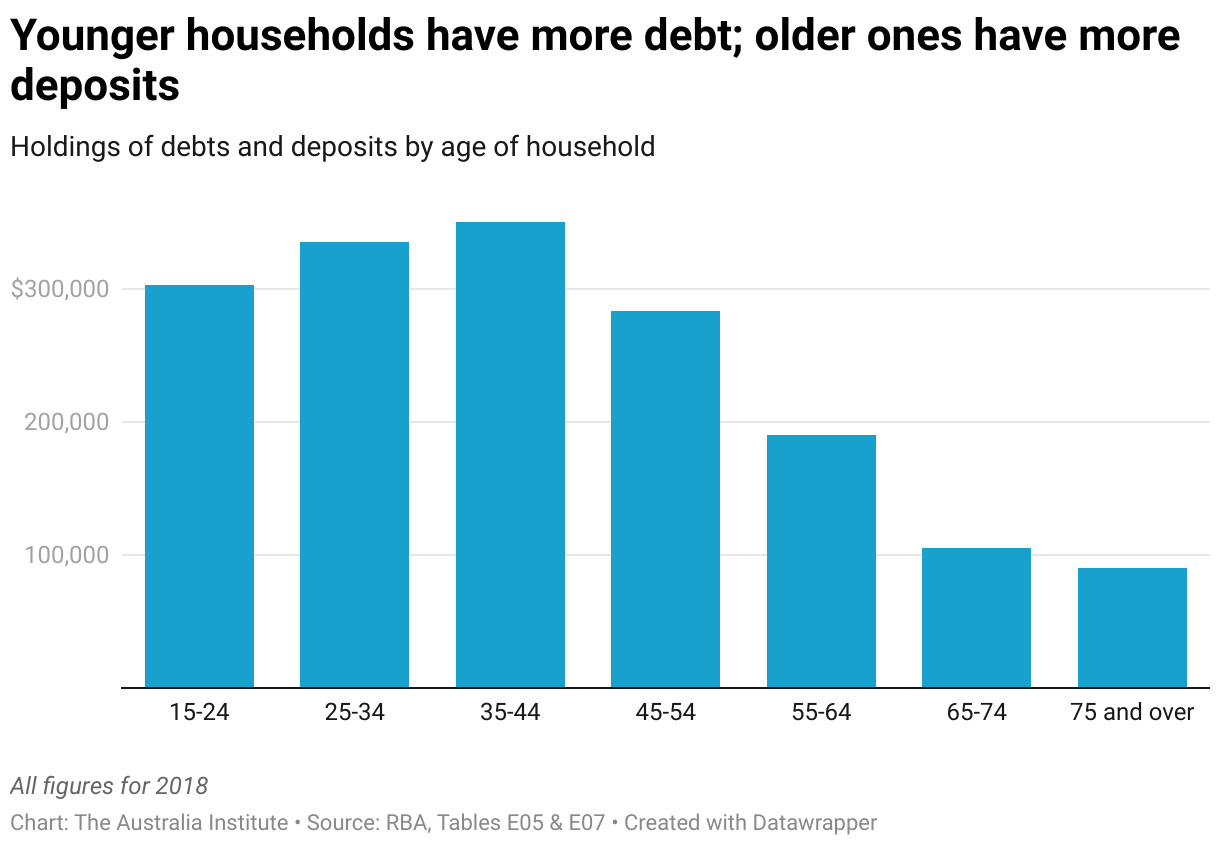

While the rate rises do also increase the amount of interest rate payments for those with term deposits and the like, the distribution of these gains and costs is very uneven – hurting younger people with new home loans and helping older retirees with larger stores of wealth. This means that the economic hurt from rate rises is not cancelled out by the extra interest paid to deposit holders. It is mostly just transferring the nation’s wealth from younger lower income and lower wealth households to richer income and wealthier households.

This $212bn extra in interest payments needs to be considered when evaluating stimulus programs or spending. For example, the Energy Bill Relief Fund extension and expansion that was in the May Budget will cost $2.6bn this financial year. That is barely over 1% of the increased cost of the rate rises to households.

Tight monetary policy through higher rates costs the economy in an uneven way. Commentators and economists worrying about government spending causing higher inflation need to consider just how much money has been taken from households and businesses and gone to banks in the past year. And they need to realise that helping those who have been hurt is not fueling more inflation.

Related research

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

10 reasons why Australia does not need company tax cuts

1/ Giving business billions of dollars in tax cuts means starving schools, hospitals and other services. Giving business billions of dollars in tax cuts means billions of dollars less for services like schools and hospitals. If Australia cut company tax from 30% to 25% this would give business about $20 billion in its first year,