Wages are clearly not driving inflation as new data shows wage growth is falling

With wage growth already falling, further interest rate rises would only serve to punish workers who are already suffering.

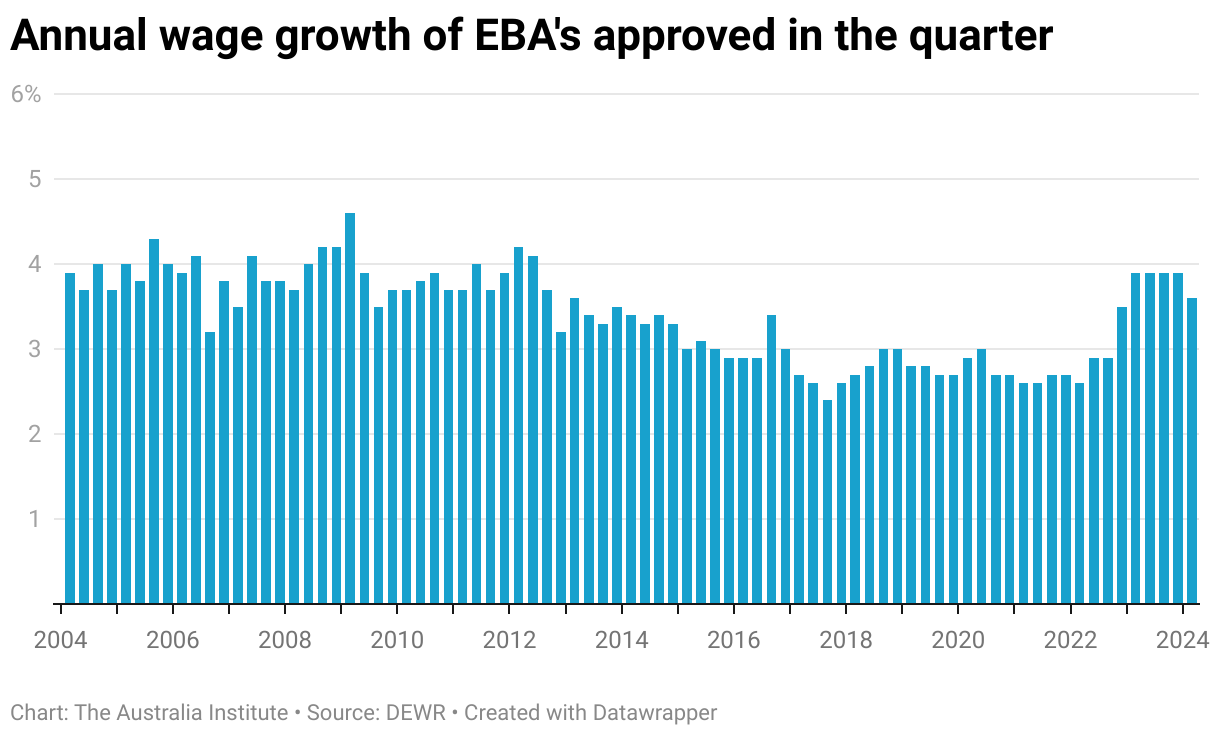

The latest inflation figures that saw annual inflation rise from 3.6% to 4.0% in May have caused some economists and commentators to argue the Reserve Bank needs to raise interest rates. However new data from the Department of Employment and Workplace Relations on enterprise agreements shows yet again that wage growth and increased income are not fueling inflation and thus an interest rate rise would do more harm than good.

In the first three months of this year, 1,022 enterprise agreements were approved by the Fair Work Commissions covering some 365,000 employees. Across all these employees the average annual wage growth of the agreements was 3.9%, down from 4.4% in the last three months of 2023.

Among private sector workers, the average agreed annual wage rise fell from 3.9% to 3.6% – a rate in line with the 3.6% annual inflation in the first three months of 2024.

The figures demonstrate yet again that wage growth has not driven inflation. Indeed a rate of 3.6% would see workers’ real wage fall after taxation and interaction with entitlements.

While conservative economists blame too much spending and strong income rises on the level of inflation, these figures highlight that workers are the ones who have suffered the most from inflation. Despite years of warnings about wage-price spirals, all we have seen is the real wages of workers decline. The 3.6% annual wage growth is perfectly in keeping with long-term inflation and productivity growth. It also is currently at a level that will keep real wages at levels some 5% below what they were before the pandemic.

Workers are being told they need to accept lower wage growth for the good of the economy, despite having been the ones who were the victims of the price rises rather than the creators of the problem.

The Reserve Bank raises rates to reduce the ability of people to spend which in turn raises unemployment. This increase in unemployment will then, in theory, reduce wage growth, which will then, supposedly, reduce inflation. However, such a theory misdiagnoses the problem. Wages are not causing inflation. Any further interest rate rises will only serve to reduce already weak demand in the economy and risk unemployment rising at rates consistent with a recession.

Both the government and the Reserve Bank should work to keep unemployment below 4% and not punish workers through higher interest rates.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

The Wage Price Index shows pay packets are up. So why doesn’t it feel that way?

The latest figures from the Australian Bureau of Statistics show wages are growing at a reasonable rate, but a deeper look shows a big problem might be about to bite Australian workers.

When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?

Productivity has grown, so why have wages not kept up?

Productivity growth is supposed to be the key to boosting wages and living standards in the economy. However, just as housing price growth decoupled from wage growth in recent decades, new research shows that real wages have not kept up with productivity growth. So, who is getting the benefit? Firstly, it’s important to understand productivity. Productivity