When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?

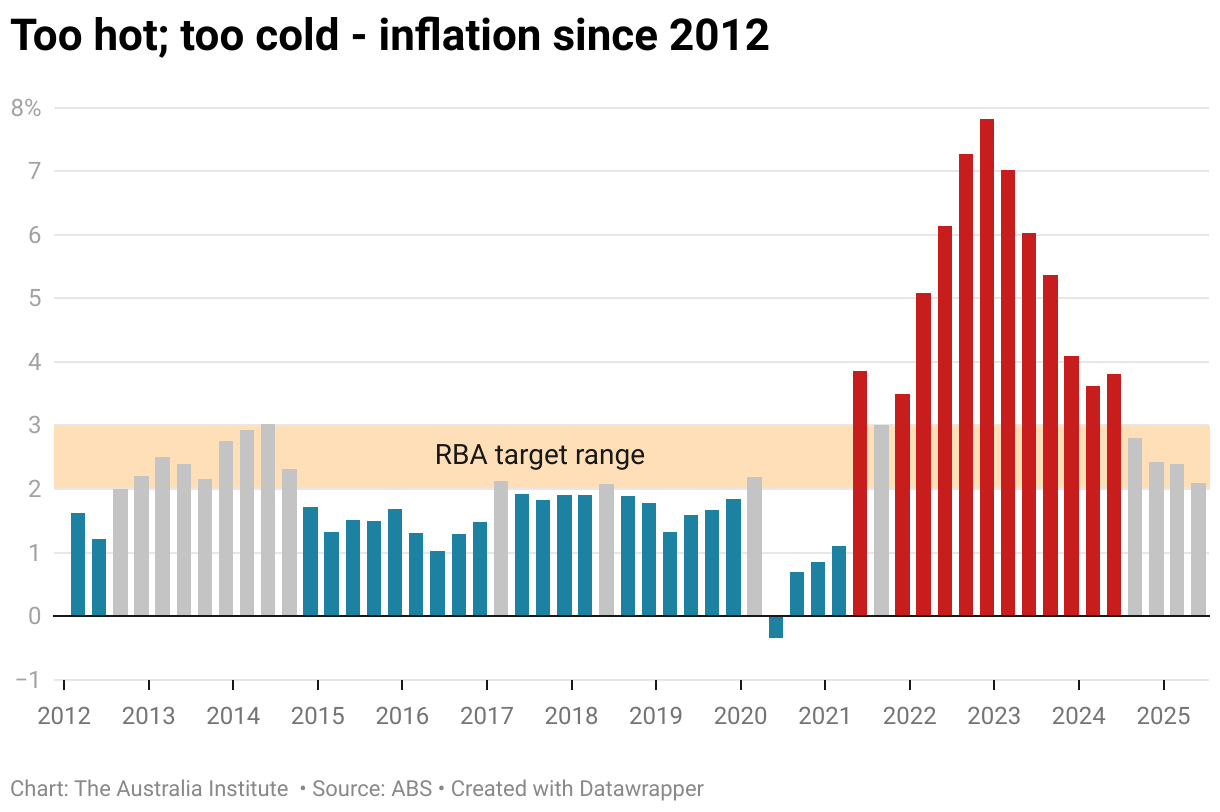

The Reserve Bank of Australia (RBA) has a target to keep headline inflation between 2% and 3%. By any reasonable measure it has completely failed on this over the last decade.

The June quarter released this week shows that inflation has been within the band for the last four consecutive quarters. This is the first time we have seen four consecutive quarters in the RBA target band since 2014.

Since the end of 2014 there have been just eight quarters where inflation has been in the target band and half of those are the four most recent ones. That means just eight of the last 43 quarters have been in the band. How can that be judged as anything but a complete failure?

Most recently, the inflation rate has been higher than 3%, but for most of the past decade, it has been outside the band because it has been below 2%.

In the 43 quarters since December 2014, inflation has been too high for 12 quarters, but too low for 23 quarters.

You might think that inflation is bad, and so having inflation below 2% is a good thing. But there is a reason that the RBA inflation target has a lower limit.

Low inflation comes with sluggish economic growth and higher unemployment. The 2022 RBA review actually rebuked the RBA for not doing enough to increase inflation in the years before the pandemic. They said that the RBA had kept interest rates too high for too long when inflation was below 2% which resulted in more people being unemployed.

Remember the RBA is not just supposed to keep inflation within the band, they also have an objective to maintain full employment.

Throughout the inflationary spike following the pandemic the RBA has talked tough on getting inflation back to target. The board statements has frequently noted “The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.”

The fact that inflation spiked after the pandemic and was above the target band was not the fault of the RBA. This spike in inflation was worldwide and was caused by factors far beyond their control.

But actions speak louder than words and the past 10 years have highlighted that they show a lot of concern when inflation is above the band and too little concern when the inflation is below the band. This means they have not shown enough attention to the employment side of their mandate.

This history is important because there is now a real risk that the RBA will fall back into bad habits. The most recent quarterly inflation data in June 2025 shows inflation has fallen to just 2.1%, the very bottom of the target band. The monthly inflation for June was just 1.9%. It is important to note that the monthly inflation figures are not a complete read on inflation like the quarterly figures.

Despite this, the RBA seems more concerned about a sudden outbreak of inflation that might push inflation back up above 3%, than the risk that unemployment might rise. Has the RBA failed to heed the review? Will it allow inflation to fall below 2% and for unemployment to continue to rise?

If the RBA lets inflation fall too low, then people will lose their jobs, and those with mortgages will continue to be squeezed. We can’t go back to the failure of the pre-pandemic period.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.

RBA wrong to punish workers for rising inflation – new report

Workers are being unfairly punished for increasing inflation, according to a new report by The Australia Institute.