Over the next few weeks, the Reserve Bank will ponder just how strong the economy is.

And if it focuses on the labour market, unfortunately the signs are that things are not strong at all.

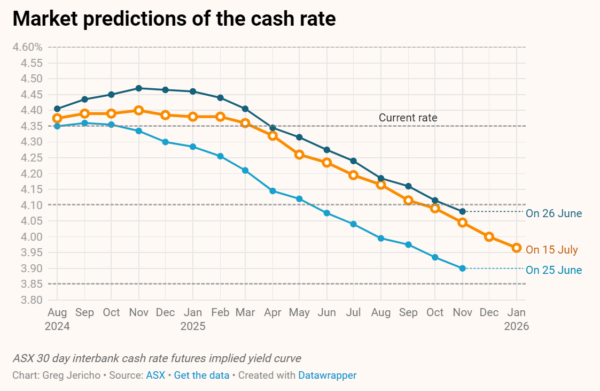

In some good news for homeowners and those worried about the RBA sending the economy into a recession, even after the surprisingly high May inflation figures, investors have little expectation that the Reserve Bank will raise rates in three weeks’ time:

But the talk of a rate rise remains, even though the economy itself is struggling. Just yesterday the IMF revised down predictions for economic growth this year from 1.5% to 1.4%.

With unemployment at 4.0% (the June figures will come out later on Thursday), are things not doing OK?

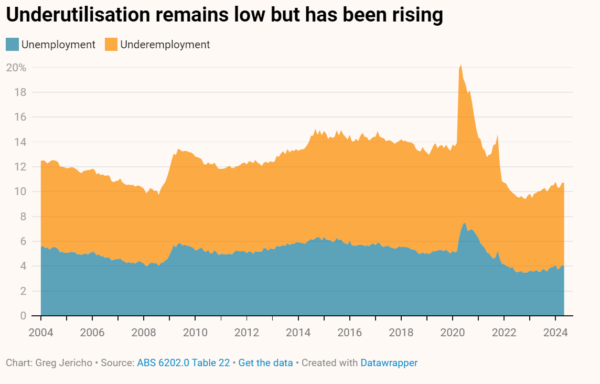

Yes, but including underemployment, which has been rising, the level of underutilisation (which counts both unemployment and underemployment) has risen from a low of 9.5% in February last year to 10.7% in May.

While that is lower than we have experienced for over a decade, it suggests that jobs are now harder to get.

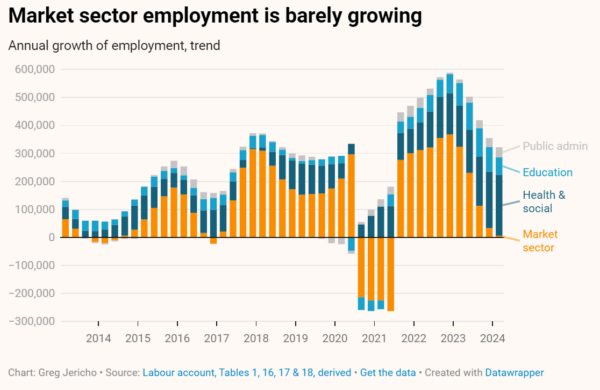

And when we break down the numbers further, the strength of the labour force reflected through the low unemployment rate seems rather fragile.

Commonwealth Bank economists posted an interesting graph that highlighted how jobs are mostly coming from the public and non-market sectors:

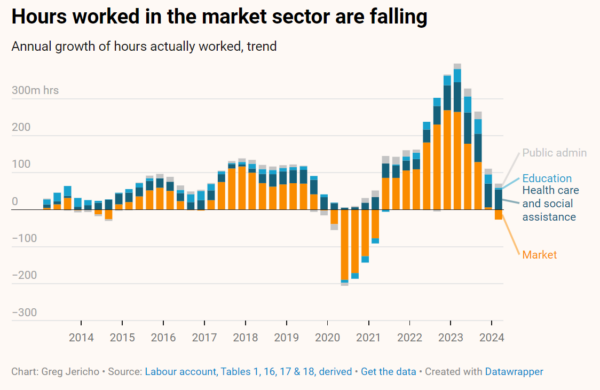

Excluding public administration, healthcare and social assistance, and education and training, total hours worked has actually fallen in the past year:

That overall employment is holding up and unemployment is remaining low is clearly good, but that this is largely being driven by public-sector work – and especially jobs under the NDIS – does not suggest a booming economy in dire need of slowing.

And you might have noticed that at this point I have only focused on jobs and not on cost of living or inflation. While these are front-of-mind for people, inflation does not actually tell us much about how the economy is faring.

It’s for this reason that I have never put too much store in things such as the “misery index”, which combines inflation and unemployment to give a measure (supposedly) of how miserable we all are.

With inflation and unemployment both at 4.0%, the misery index for Australia is 8.0%. That is the same as a decade ago, when inflation was 1.7% and unemployment was 6.3%. If anyone thinks Australians would be no less miserable if we had an extra 343,000 unemployed but with lower inflation, please feel free to volunteer your job to the cause.

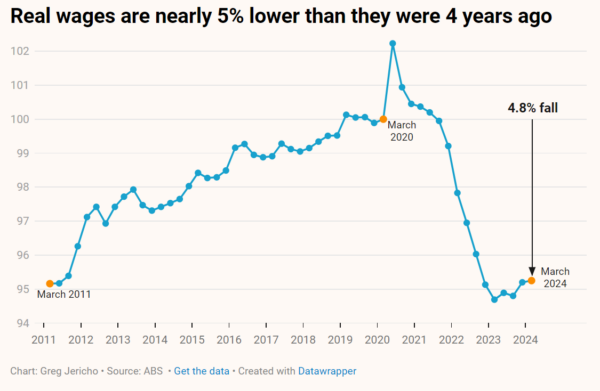

If inflation was being driven by a booming economy we would also expect to see wages surging. And yet wage growth has peaked and real wages are barely growing at all.

On this score it was good of the OECD to remind us that workers have seen their living standards destroyed over the past couple of years.

In its latest employment outlook, the OECD noted that real wages have fallen more than most other economies and “are still 4.8% lower than they were just before the pandemic” in December 2019.

To underline how massive that loss is, note that 4.8% of $80,000 is $3,840.

So when you hear that real wages have fallen by 4.8% that is like hearing someone on $80,000 losing nearly $4,000 worth of services and goods that they were able to afford in 2020 but cannot now.

While wages are finally growing faster than prices, the OECD noted with superb understatement that “households are still facing pressure under the cost-of-living crisis”.

This of course comes down to interest rates. Interest rates slow the economy, by making it tougher for consumers to spend money in shops and on services, and thus harder for businesses to hire more workers because the work is not there.

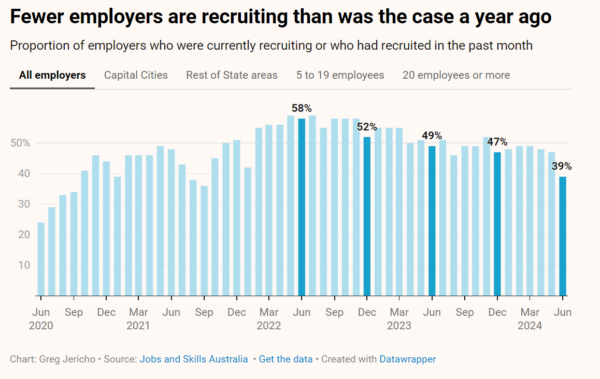

When we think of it this way it seems rather obvious why market sector jobs are not growing. Worse still, the signs are that there is little good news ahead.

In June just 39% of employers recruited new staff – down from 47% at the end of last year:

And only 18% of employers were expecting to increase their staff in the next three months – down from 20% in December last year and 21% a year ago:

This again is a sign not of an economy needing to be restrained but one that has slowed and, rather than about to rebound, is set to slow even further.

That will be good news for those who are suffering from rate rises because it suggests the Reserve Bank will be unlikely to raise rates in August.

But the bad news is that even if the RBA keeps rates on hold, the impact of all the rates rises continues to flow through the economy. For now, unemployment has remained low but the chance that it will start rising is becoming rather more likely than it once was. And a further rate rise would only make that chance almost certain.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Feeling hopeless? You’re not alone. The untold story behind Australia’s plummeting standard of living

A new report on Australia’s standard of living has found that low real wages, underfunded public services and skyrocketing prices have left many families experiencing hardship and hopelessness.

BREAKING: Australia’s housing market still cooked

Even the Mathias Cormann-led OECD says the capital gains tax discount and negative gearing are a problem.

Greg’s budget wishlist

The Australian Government can’t afford to do everything, but it can afford to do anything it wants.