Last week before the House Economics Committee, the Governor of the Reserve Bank made it clear that the current rise in inflation has nothing to do with wages growth. And yet he also made it clear he expects workers to bear the brunt of the cost that comes from slowing inflation.

In his Guardian column, Policy Director Greg Jericho notes that given real wages have already fallen for 2 straight years any further falls will take workers’ purchasing power backwards to where it was more than a decade ago. This however is viewed as being “worse than the alternative” of inflation growth above 3%.

He notes that over the past 2 years the profit margins of many industries, and most especially the mining industry, have risen and have themselves fuelled inflation. But company profits are never expected to suffer, wages however are always viewed as either the culprit of inflation or the means to reduce it. The vast increase in mining profits, largely due to the Russian invasion of Ukraine, also highlights the urgent need for a windfall profits tax.

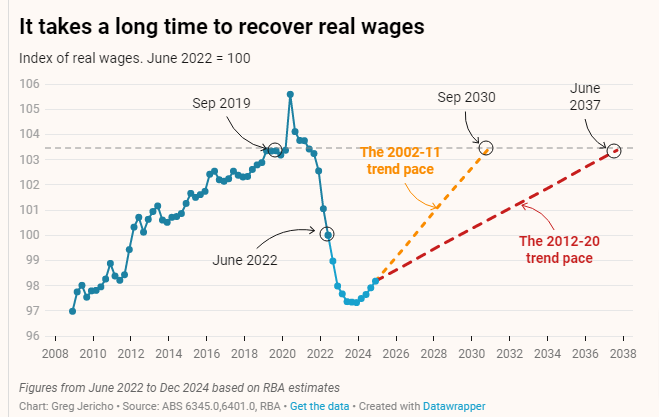

Using the RBA’s own estimates Jericho calcuates that by the end of next year real wages will be back at 2008 levels and even with the most optimistic outlook they will not return to 2019 levels until 2030.

The Reserve Bank’s strategy of sharply increasing interest rates risk slowing the economy into a recession even though real wages are already falling faster and for longer than they have in modern times.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

When targeting inflation, the RBA misses more often than it hits

With the fight against high inflation now over, will the Reserve Bank fail to learn the lessons of the past and allow inflation to fall below 2%?

Fearful and frozen: Why the Reserve Bank continues to err on rates

The RBA’s failures have real consequences. It should go back and closely reread the recommendations of the RBA review, particularly the ones that encourage it to open up to new and diverse viewpoints.

Corporate Profits Must Take Hit to Save Workers

Historically high corporate profits must take a hit if workers are to claw back real wage losses from the inflationary crisis, according to new research from the Australia Institute’s Centre for Future Work.