In the past 7 months, the Reserve Bank has increased the cash rate by 275 basis points. That is as fast as any time since the RBA became independent. Given the pace of inflation growth, the rises are not wholly without cause, but as policy director, Greg Jericho notes in his Guardian Australia column the main drivers of inflation are now easing, and wages are yet to take off. In that case, should the RBA continue to raise rates given it will only slow the economy further?

Over the past year, the main driver of inflation has been house prices accounting for a quarter of the 7.3% rise in the CPI. And yet we know that house price growth is now either slowing dramatically or even falling in some areas. The RBA has also noted that commodity prices are falling and supply-side issues are being dealt with and that these aspects, which are not influenced by interest rates, will reduce inflation next year.

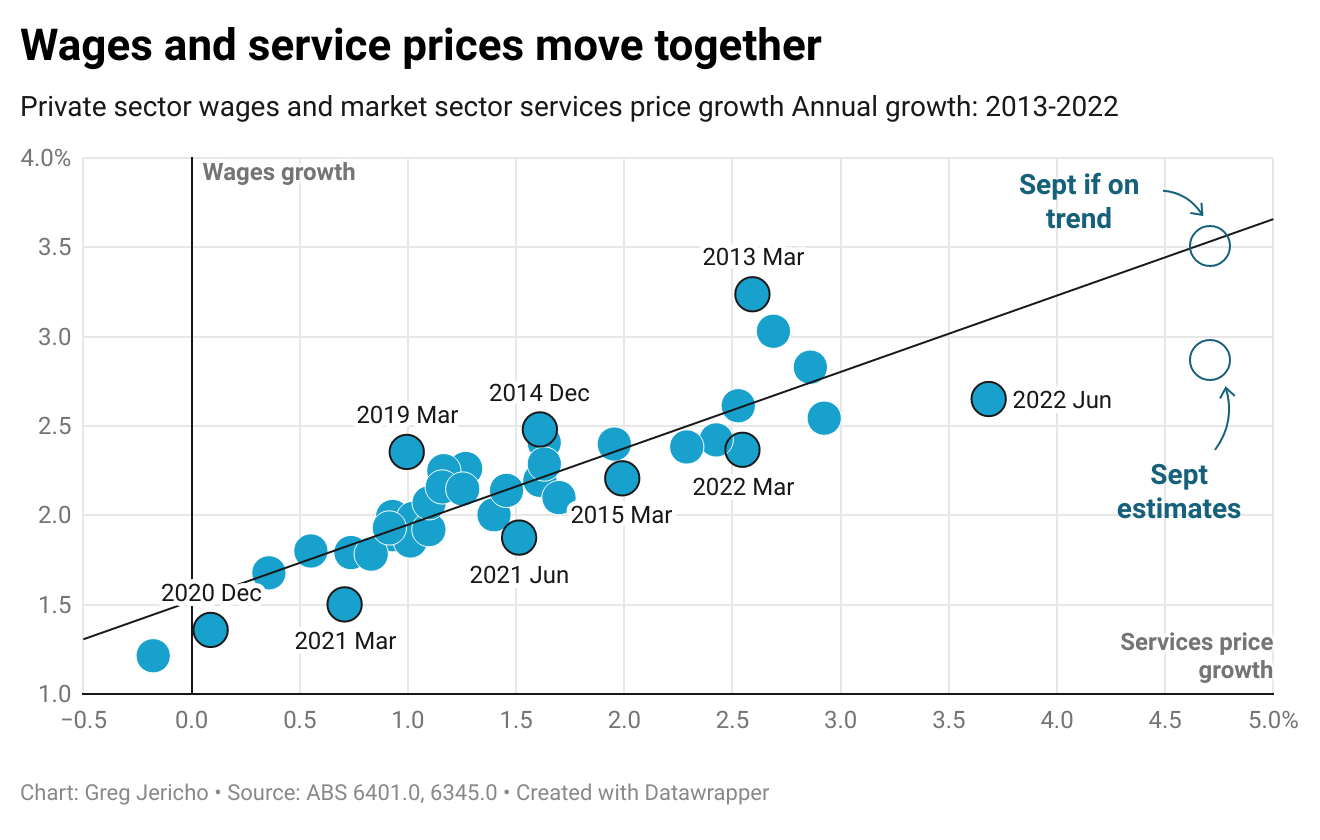

At the same time, the Reserve Bank continues to sound warnings of a wage-price spiral despite any evidence of such a thing occurring. Indeed the latest CPI figures show that overwhelmingly inflation is driven by the price rises of goods rather than services. This is important because service prices and wages are strongly linked.

More rate rises will certainly continue to reduce demand in the economy as the cost of servicing a mortgage rises. But to what end? The main factors driving inflation are easing, wages have not risen above 3% yet, let alone to a rate anywhere near inflation.

Even if wages were to rise in line with the historical link with service prices, in September they would have risen 3.5% – a level very much consistent with inflation growth of between 2% and 3%. And yet we know that wages are unlikely to rise that fast. The most recent estimates have it closer to 2.8%.

The great risk now is that further rate rises will only hurt the economy for little gain and see wages growth stunted before they even get to a level that would see real wages rising.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.

Budget 2026: Housing changes to slowly reverse decades of damage

The government’s changes to capital gains and negative gearing will begin to undo decades of damage to the housing market caused by Howard-era policies – so will Elinor actually be able to buy a house?

Shame and harm at every JobSeeker turn – and now with added AI slop

“Single JobSeeker [payment] just hit $400 a week. Let me know how you’d go if you were getting that little and were randomly not paid.” This comment, from the people behind Nobody Deserves Poverty, points to the ignored cruelty at the heart of one of Australia’s most shameful open secrets. The mutual obligations system –