Budget Wrap-Up

Commonwealth Treasurer Scott Morrison tabled his 2017-18 budget in Parliament House on May 9, and the Centre for Future Work’s Director Jim Stanford was there in the lock-up to analyse its likely impacts. Here are some of our main impressions and comments:

Wage Growth and Deficit Reduction

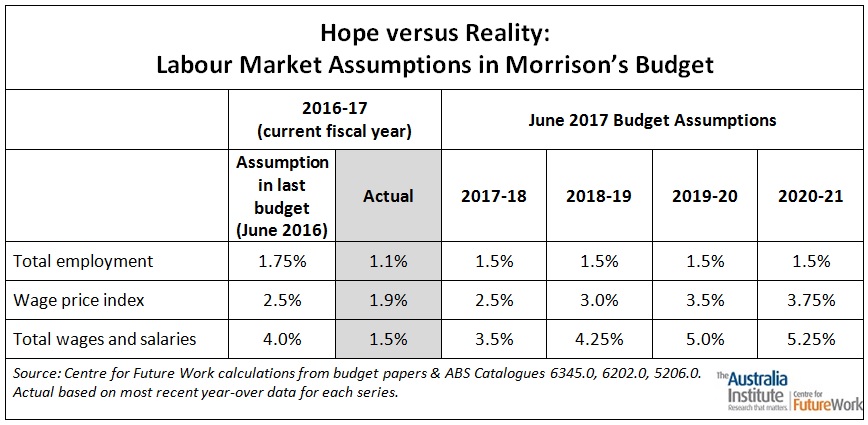

Several commentators have highlighted the budget’s highly optimistic assumptions regarding future job-creation and wage growth incorporated into the budget forecast. The government is anticipating an immediate and sustained acceleration of all of the factors that contribute to the wage base for tax revenue: faster job-creation, significantly faster growth in hourly pay, and dramatically faster growth in total wages and salaries.

Back in the real world, the labour market has been underperforming on ALL THREE of those components: slow job-growth, record slow growth in hourly wages, and falling weekly hours of work (due to the dramatic expansion of part-time and irregular work). For all of these reasons, total wages and salaries paid out in the economy (which forms the major basis for personal tax collections, both income and GST) actually declined in the latest quarter of GDP (Dec 2016).

This table summarises the main wage assumptions in Mr. Morrison’s budget, contrasting them to the latest actual figures on each of the three criteria. The last budget (2016-17) missed the mark badly on all three criteria — but the likely undershooting error will be huge by the end of this budget’s forward estimates, unless there is a dramatic and sustained acceleration of employment and wages growth.

Director Jim Stanford pointed out in this Huffington Post column that the current weakness in Australian wages is not an accident, nor is it likely to reverse automatically. Chronically weak aggregate labour market conditions, combined with structural attacks on the institutions that support wages (including unions, minimum wages, penalty rates, and others), have caused the unprecedented stagnation of wage incomes in Australia. The macroeconomic consequences of this state of affairs have been widely acknowledged — even by the government itself. (Mr. Morrison himself spoke recently of his concern with the impact of wage stagnation on his own budget targets.)

As Stanford put it in his Huffington Post commentary, the contradiction between the government’s wage-suppressing economic and regulatory policies, and its hope that wage growth will nevertheless power the way to a balanced budget, is both glaring and unsustainable:

“[Morrison’s] rose-coloured labour market assumptions will be sabotaged by his own government’s continuing war on workers and wages. And that’s one important reason why his hopeful deficit targets will not be realised.”

General Optimism Regarding Revenue

The budget’s optimistic wage growth assumptions are just one factor behind an overall revenue forecast that is downright ebullient. The main force behind the projected return to a balanced budget is an enormous assumed increase in tax revenues — very ironic coming from a government that regularly derides the alleged “tax-and-spend” procilivities of its opponents. Over the four years of the forward projection, annual revenues are expected to expand $120 billion by 2020-21 (or 30 percent). As a share of GDP, revenues are expected to swell by 2.2 percentage points, reaching the highest share (25.4% of GDP) since the peak of the mining boom (in 2005-06).

There is no clear explanation of where these huge new revenues come from – especially given the revenue-reducing effect of other budget measures, including company tax cuts, the elimination of the deficit repair levy for high-income earners, last year’s bracket adjustments, and others. There are some modest revenue measures in the budget: including the 0.5% Medicare levy increase (after 2019), the levy on bank liabilities, and a new levy on employers who hire migrant labour. But those policy decisions account for just 6.5% of all new revenues assumed to be received over the coming 4 years — and they will be more than offset by the revenue losses from the other measures (especially the company tax cuts).

If revenues stay constant as a share of GDP (instead of magically growing), the budget will be $45 billion short in 2020-21 – and the forecast small surplus will evaporate into a large continuing deficit. Indeed, as our colleagues at the Australia Institute have pointed out, this budget marks the fourth consecutive four-year LNP timetable for balancing the budget. The government’s tough talk on the dangers of deficit-financing, and stated intention to quickly achieve balance, have proven hollow. Many of its proposed spending cutbacks have been successfully resisted by community campaigning. And its rosy revenue forecasts have been consistently unfounded. There is no reason to believe this year’s four-year deficit elimination timetable is any more realistic than the last three.

Robbing Peter to Pay Paul

On the spending side, the government is announcing some modest new spending initiatives, totaling $9 billion over 4 years.

But at the same time, they are announcing spending cuts to a wide range of programs (including higher education, welfare, and civil servants) – totaling $10 billion over the same period.

The net impact of new policy decisions on spending is therefore $1 billion in the negative. Despite the promise of “better times” in the future, the government’s discretionary actions will reduce aggregate funding for the programs that Australians depend on.

A Target Everyone Can Love: The Big Banks

The government’s new 6 basis point “levy” on bank liabilities (ie. on outstanding loans) is forecast to raise $6.2 billion over 4 years.

Many analysts believe this tax will be passed on to borrowers (since it is defined as a proportion of lending), and the government has not provided a convincing refutation of this concern. The levy is equivalent to a slight increase in the cost of capital for new lending. (In fact, this new “levy” is smaller than recent increases in interest rates which the banks have already passed on to their borrowers.)

The government’s claim that the ACCC, with increased funding, will ensure the banks do not pass on the costs of the levy is laughable — as is its claims that competition from smaller banks will keep the big banks in line. Unless there is outright collusion and price-setting between the banks (something that is rare and unnecessary anyway), there is nothing illegal about passing on higher costs to consumers. Indeed, the ability to do this is precisely what explains the banks’ consistent above-normal profits (earning return on equity of 15 percent or more each and every year).

At any rate, once the banks start to benefit from the full 5% reduction in their own corporate taxes (by 2026-27), they will still be saving billions each year on a net basis.

The eminent economist Prof. Geoffrey Harcourt, a good friend of our Centre, put it this way in a blog comment:

“The discussions on the levy/tax on the big four banks in the 2017 budget are often hysterical and beside the point. Because banks play an essential role in the running of the economy, they need protection through a guarantee from the government. Because of their oligopolistic market structure, they are in a privileged position to make large profits, a portion of which reflects their necessary privileged position, rather than any merit of their own. Common sense suggests that it would be both efficient and equitable that the banks be allowed to receive, say, the average rate of profits ruling in the economy as a whole without being taxed differently than any other form of enterprise in Australia. If their overall rates of profit are greater than the average – which they certainly are – the differences between the two sets of rates should be subject to a higher rate of tax so that the community at large receives a return on the privileged position the banks have been necessarily granted. The proposed levy is roughly akin to this proposal, which is tackling an equitable puzzle. It should not, in principle, be related to what is happening to the budget overall and especially to the sizes of any deficits or surpluses. These should reflect the outcome of attempting to meet the real aims of good government starting with achieving and sustaining full employment and sustainable growth.”

Infrastructure Spending: Show Us the Money

The government is boasting of $75 billion in infrastructure funding and financing over the next ten years. It is impossible to know how much of this represents new funds, nor when the funds would be delivered. Keep in mind that at present the government already spends over $18 billion per year on capital (or $200 billion over the next decade): both on new projects, and offsetting the wear and tear of existing assets. So the $75 billion “plan” ($7.5 billion per year) may or may not represent a substantial ramp-up in new capital spending by Canberra.

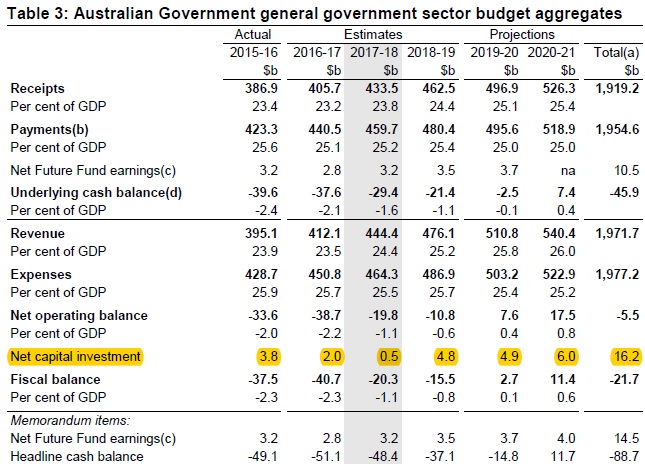

In fact, the details of the budget do not seem to indicate any enormous expansion in capital spending. Net capital spending (after depreciation) is projected to decline in 2017-18: to just $0.5 billion, the smallest since 2002-03. (See Budget Table 3, reprinted below.) In essence, in the first year of the budget, the government will spend barely enough to offset depreciation of existing assets.

Net investment grows in later years, but not dramatically. And as a share of GDP, net capital spending by the Commonwealth is projected to average just 0.2% of GDP over the forward projections. Over the last ten years, in contrast, it averaged 0.25% of GDP. In other words, under this budget, net Commonwealth capital spending will actually shrink relative to the economy.

It is easy to come up with “big numbers” when talking about infrastructure programs (especially by summing totals over many years), and associated ribbon-cutting ceremonies will attract much attention. But there is no concrete evidence that this budget will accomplish the real and sustained increase in Commonwealth government capital spending that is needed. Commonwealth capital spending has declined in recent years compared to earlier decades, and there is no evidence that this budget will change that trend.

Migrant Labour and Apprentices

The government is imposing a new “head tax” on employers who hire foreign migrants: $1200 to $1800 per year per head for temporary migrants, and $3000 to $5000 for each permanent migrant (on a one-time basis). The revenues from this levy will be used to fund support for apprenticeships in conjunction with the states, to a total of $1.2 billion over the next 4 years.

Funding skill programs through a tax on migrant labour is not an effective way to rebuild Australia’s battered vocational education system – nor is it an effective way to regulate employers’ over-reliance on temporary foreign migrants (rather than recruiting and training Australian workers). Indeed, the scale of revenues anticipated by the government suggests that incoming migrant labour will continue to constitute a major force in Australia’s labour market.

Effectively regulating and reforming Australia’s migrant labour system – limiting its use to classifications where skilled workers are truly unavailable, and ensuring that migrant workers are entitled to the same protections as all other workers – would in fact undermine the head tax revenues that the government is now counting on.

Check Out The Australia Institute’s Budget Analysis

Our colleagues at the Australia Institute have also generated some useful and punchy commentary on the budget: see it all (including a hilarious podcast with economists Richard Denniss and Matt Grudnoff) on the Institute’s Budget Wrap page.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

Centre For Future Work to evolve into standalone entity

The Centre for Future Work was established by the Australia Institute in 2016 to conduct and publish progressive economic research on work, employment, and labour markets. Supported by the Australian Union movement, the centre produced cutting edge research and led the national conversation on economic issues facing working people: including the future of jobs, wages

Go Home On Time Day 2025. As full timers disconnect, part timers are doing more unpaid overtime

New research by the Centre for Future Work at The Australia Institute has revealed a disturbing new twist when it comes to unpaid overtime in Australia.

A smooth move or a tough transition? Protecting workers who’ll lose their jobs when the Eraring Power Station closes

The Centre for Future Work at The Australia Institute has urged the federal government to take charge of transitioning hundreds of workers into secure employment when the Eraring Power Station shuts down.