The Australia Institute’s Budget 2017 Wrap

Our team of economists and researchers have cast their eye over a range of areas — some of the ‘big ticket’ items, and some the Government were probably hoping to sneak by without anyone noticing.

Listen to our Follow the Money podcast Budget Special

The Australia Institute Deputy Director, Ebony Bennett, caught up with Senior Economist Matt Grudnoff and Chief Economist Richard Denniss as they emerged from the budget lockup to record this quick Pocket Money edition of Follow the Money.

Listen here → ‘Follow the Money’ 2017 Budget Special or on iTunes here.

Farewell Abbott & Costello

By Richard Denniss, Chief Economist

The year is 2017 and the Treasurer of Australia is going to collect more tax. It turns out taxes are not actually a “burden”, but a necessary revenue-raising measure in order to fund projects Australians want. Who knew?

It took 10 years, but Peter Costello’s legacy no longer haunts the budget. Ironically, it was his own side of politics that finally exorcised the boom-time doctrine that tax cuts were the only way to stimulate the economy. There is no mention in Scott Morrison’s second budget speech of the ”burden” of tax.

The 2017 budget represents the fundamental repudiation of Costello’s fiscal strategy and the complete abandonment of Tony Abbott’s political strategy. Morrison has offered a new tax on the big banks, a new 0.5% Medicare levy and a range of new housing policy measures that, while not as simple or effective as reforming negative gearing or the capital gains tax discount, will net the government a tiny $1.1 billion over the next four years.

In the era of good and bad debt, it now seems that all government spending is an ‘investment’ and only proposals from Labor will need to be chalked up on the “bad debt” side of the ledger. Having embraced Keynesian economics principle that public spending, not tax cuts, boost economic activity, Morrison has gone all in. His budget speech assures us that his government is proud of “investments in science and innovation”, he assures that he “will invest an additional $115 million in mental health” and of course he believes that “it is important to invest in infrastructure”.

Gone are the Costello days when spending was a drain on the economy that “crowded out” the private sector. The modern Liberal Party assures us that it “will continue to invest record amounts in education”. You get the picture.

But while the Turnbull government is pivoting radically from the themes of its last three budgets, there is still no indication that they are willing to jettison their most expensive baggage. While there is an unexpected great big new tax on the biggest banks, the Turnbull government seems determined to stick to its uncosted plans to slash the corporate tax rate. For the big banks it seems that the Tax Office giveth with one hand and taketh with the other.

The Ugliest Debt

The Treasurer declared “this budget is about making the right choices to secure the better days ahead”. No mention of climate change, nor of his government’s decision to “invest” $1 billion in Adani’s enormous new coal mine.

Now that that the ghost of Costello has finally left the building it seems politicians from all parties can now get on with a good old-fashioned democratic debate about better and worse projects and policies to spend the money on. Poll after poll suggests handing billions for big new coal mines is right at the bottom of Australian taxpayers’ wish-list.

ABC quietly cut again

Remember Tony Abbott’s claim of no cuts to the ABC and SBS? Of course that wasn’t true and this budget does nothing to reverse these earlier cuts. Spending on ABC and SBS operations and transmission will decline by $43 million from $1,461 million in 2016–17 to $1,418 in 2018–19.

Perhaps Malcolm Turnbull’s claim to be a small ‘f’ friend of the ABC is what helps ABC and SBS funding to recover in 2020–21 to $1,453 million, just $8 million less than the start of this budget period. The ABC and SBS will need a boost in future budgets if they are to get back to 2016–17 levels in the next four years.

What the HECS? No HELP for students

By Tom Swann, Researcher

This government was so eager to exorcise the ghosts of Abbott’s education austerity, they announced their main education budget measures in advance of the budget. The big ticket item is returning some of the Gonski schools funding, to be distributed on a needs-basis. Labor points out this is still a massive a cut (-$22 billion) from the full Gonski. They also argue it will break existing deals. While few tears will be shed for cuts to elite private schools, other private schools are also unhappy, although at least one private provider is welcoming the changes as fair.

Education Minister Simon Birmingham has also tried to clear up Pyne’s higher education mess. Fee deregulation is now finally taken out of the budget, although other parts of Pyne’s proposals including big funding cuts are merely delayed, suggesting they could be resurrected. In the meantime, there’ll be an increase to university fees and a drop in the income threshold at which graduates start repaying, resulting in over $350 million in annual ‘savings’ a year from increased graduate payments. There is also an “efficiency dividend”, or cuts to funding. Overall public spending on higher education falls by $500-$600 million year.

While designed to seem modest by comparison the 2014 package, the impact of these changes are clear in the government’s targets for HELP debts, held by university and vocational graduates. Average HELP debt goes up, as does the average time to repay it, despite the new increases in repayments and students repaying more of their debt. All of this is based on wage growth assumptions that predict a huge decline to suddenly reverse. If that turns out wrong, the impacts will be greater.

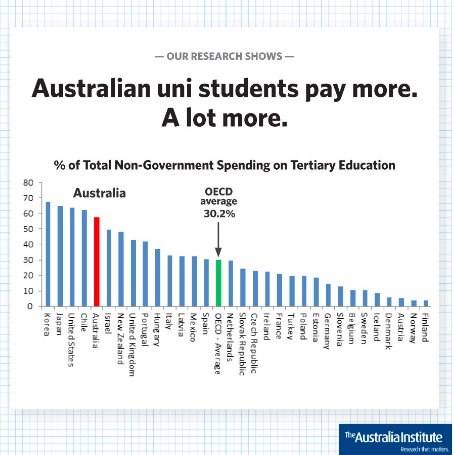

The Government wants Australian uni students to ‘pay a bit more’. The Australia Institute research shows they already contribute a lot more to the cost of their education than most OECD countries.

Of course, the impacts will be greatest for those on low incomes, making the system less progressive. Two law graduates both leave uni with the same HELP loan; one becomes a corporate lawyer and barely feels the impact of these changes, the other becomes a community lawyer and definitely will. And with no effort to address the growing shortfall in research funding, universities will keep using student fees to cross-subsidise research.

There are also measures to tie grants to accountability measures and increase reporting and transparency, alongside large cuts to higher education programs for equity of access and quality. Sub-degree diploma places will attract subsidise and there is funding for regional higher education ‘hubs’. But the big news for vocational training is a new $1.5 billion Skilling Australians Fund to fund apprenticeships, traineeships etc, to target skills shortages. This is to be funded out of a new levy on employees who bring in foreign workers; other employers will not be paying to help address these skills shortages. At the same time, there’s also $247.2m cut from the Industry Skills Fund.

The ‘Path to Surplus’ is paved with wage growth unicorns

By Matt Grudnoff, Senior Economist

Like someone who always says they will start their diet tomorrow, the budget surplus is always four years away. This is the current coalition government’s fourth budget and they have talked in each of them about a path to surplus. Despite this the budget deficit this year is almost identical to the budget deficit last year. And the budget deficit last year is almost identical to the budget deficit the year before that. And while economic predictions are always risky, I think there is a fair chance that the budget deficit next year is going to look surprisingly similar to this year’s deficit.

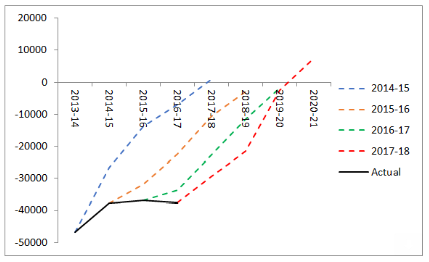

Of course the budget papers tell a very different story (as they do every year). They tell the story of a rapidly decreasing deficit and then a surplus in 2020–21. So let’s compare the four different stories from this governments four budget papers.

The Fourth 4-year plan to return to surplus

The black line shows the actual budget deficit. The dotted line shows the government’s predicted ‘path to surplus’ in each budget.

The black line shows what the actual budget deficit was. The dotted coloured lines show the ‘path to surplus’ in each budget. We can see that the budget deficit never really changes.

The predictions of a reduced deficit just shuffle along each year.

The Wage Growth Unicorn

So how does the Treasurer get the predication so wrong each year? Well the trick is to assume big growth rates in future years. This gets us to the wage increase unicorn at the centre of this budgets prediction. The wage increase unicorn is the magical creature that the Treasurer desperately wants to believe in, despite all the evidence to the contrary.

High wages growth flows through to people paying more income tax which is the extra revenue that the budget assumes will reduce the deficit.

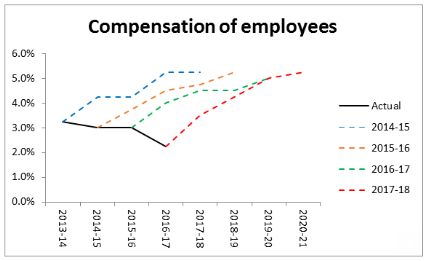

So what kind of wages growth is the government predicting? Well it’s not so much wages growth as a wages explosion. The government is predicting compensation to employees to grow by 5% or more in the last few years of the forecast.

These predictions come at a time when we have record low wages growth. It comes at a time when the government is cutting penalty rates and when the government has effectively frozen the wages of many public servants. A long term concerted push to decentralise the labour market has reduced the power of workers and reduced their ability to increase wages.

Much like the surplus, the government has consistently been predicting a pickup in wages growth. Instead we have seen compensation to employees (the amount of money going to workers) fall. Below is a graph that shows all this governments predictions (dotted coloured lines) and the actual outcome (black line).

Projected vs Actual Wage Growth

The dotted line shows the budget’s forecast for wages growth. The black line shows the actual wages growth.

We can see the budget is constantly predicting a recovery in wages while actual wages growth continues to fall.

So why does the government assume that wages will increase so fast? It is simply down to an assumption in the Treasury model that wages growth will return to the long run average. Since wages growth is currently so far from the average, the model has to assume faster growth to get back to the average. So the predicted surplus is based simply on a Treasury modelling assumption about unrealistic wages growth rushing back to a long run average.

For the Treasurer the unicorn might be pretty but it’s still imaginary.

The Housing Package: No House, All Packaging

It is almost as if the government panicked after announcing it was going to do something about housing affordability. But having already committed to something they put forward a blizzard of policies that you have when you don’t want to do anything about housing affordability. In short the pretty packaging may look like they’re doing something about housing affordability, but closer inspection shows the box is empty.

Most of the panic probably happened when the government ruled out everything it could do to actually make housing more affordable, such as restricting negative gearing and the capital gains tax discount. They have then taped together a heap of programs that individually and collectively will have little impact on house prices.

Fixing the housing affordability crisis means slower house price growth. It means that houses need to increase in price at a slower rate than wages. Given wages are at record lows this means house prices really have to stop growing.

The government is keen to say these reforms are not a silver bullet, but in this case all that means is they’re admitting failure at the start.

This housing package is also confused. While there are some measures that may put a tiny amount of downward pressure on house prices, there are others that will do the opposite, put a small amount of upward pressure on prices.

First to those measures that might push down prices (assuming you had a microscope powerful enough to see the downward pressure).

There are a large number of measures aimed at foreign investors. This is despite the recent crackdown on foreign investors having next to no impact on house prices. While the policies might not do much the politics is far better. There is little to no political damage attacking foreigners. The new policies include restricting to 50% the amount of foreign investment in a development (the likely effect of this is force foreign investors to invest in multiple developments rather than just one). Charging a fee if foreign investors leave an investment property vacant for 6 months of the year and restricting some capital gains tax concessions that foreign owners can claim.

The government is introducing some limitations on the sorts of things investors can deduct. Investors can no longer claim travel to inspect their investment property. This was a loophole that allowed some investors to effectively get the tax payer to part fund their holidays. There is also a change that means only the original investor can depreciate portable appliances.

There is also a measure to encourage older Australians to downsize by allowing them to deposit some of the sale price of their house into superannuation. Doing this might create some problems for retirees since the family home is currently exempt from the pension assets test but superannuation isn’t. If retirees deposit some of the value of their home in their super, this might reduce the amount of the age pension they can claim. It is likely that the very wealthy, who currently don’t receive a pension will be the biggest beneficiaries of this.

While these policies might have some small downward impact on house prices there are also two policies that are likely to push house prices up. This includes a higher CGT discount for those that rent to low and moderate income tenants and the ability for first home buyers to save up for their deposit by using income that is taxed at a concessional rate.

Rather than crack down on the capital gains tax discount, which would help to push out property speculators from the market, the government has decided instead to invite more of them in by increasing the discount from 50% to 60%. The catch is that investors need to rent to low and middle income households. But as the Treasurer has said in the past “Australian residential property investment is more geared to capital gain than yield.” Basically he is saying they’re all a bunch of property speculators who are not very interested in the rental return and instead have their eye on the capital gain. Making the capital gain even bigger by further cutting the amount of tax you have to pay will only encourage more speculation.

The last policy is probably the one that has got the most attention. It allows first home buyers to put additional pre-tax income into their superannuation accounts to save for a home deposit. This is better than allowing first home buyers to use their super to buy a home, but it’s still not a great idea. You can see the attraction for first home buyers. They’re all thinking about how much faster they can save for a deposit. But the problem is that if a lot more people show up to the auction with more money in their pockets then all that happens is that the house sells for more. If this pushes up house prices then bigger deposits are required negating the advantage that saving in the super fund gave them in the first place. Of course pushing up house prices further encourages the speculators.

The governments much anticipated housing affordability package was sadly lacking in affordability. Rather than tackle the source of the problem, an over investment in residential housing, they have instead put up a confused patchwork of polices, most of which will have little to no impact on affordability. Some could even make it worse.

Houston, we finally have to admit… we have a revenue problem

It wasn’t just deficit and debt disaster that the government dumped. They finally acknowledged that the budget has a revenue problem not a spending problem. After years of pointing this out The Australia Institute is happy that the government has finally seen the light. This budget expects to see government policies raise an additional $23 billion over four years.

While the government’s actions might show they have abandoned the ideologically driven idea that you can only reduce the budget deficit by cutting spending, don’t expect the Treasurer to admit that anytime soon. Some ideological waters run deep.

The biggest of the revenue measures that the government put in place was the increase in the Medicare levy to help fund the NDIS, which will raise $8.2 billion over the forward estimates, and the new bank levy which will raise $6.2 billion also over the forward estimates.

Hopefully the government has realised that Australians are prepared to pay for high quality, fairly distributed, government services. Now they just need to give up on getting rid of the budget repair levy, which will see people earning more than $180,000 per year get a 2% tax cut and forget about their $50 billion corporate tax cut.

Another attack on the unemployed, but who’s counting

By Hannah Aulby, Researcher

Surprise, surprise, another attack on unemployed people in this year’s budget. Much attention has already been given to the forced drug testing of new welfare applicants, and hidden in this is another cut to welfare spending. The government plans to cut $632 million from unemployment benefits over the next four years.

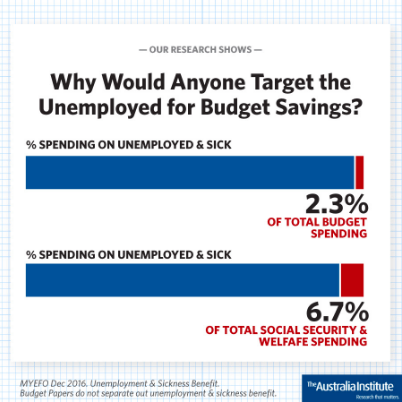

The reason? “Efficiencies from this measure will be redirected by the Government to repair the Budget and find policy priorities”. This makes it seems like unemployed people are soaking up large amounts of resources that could be better spent elsewhere. In reality, the updated numbers in the 2017 budget showed that government assistance to the unemployed and sick down to is 2 per cent of total budget spending, and 6 per cent of social security spending.

It’s not as if everyone is tightening their belts for the greater good. In fact total government spending has gone up $50 billion since the Coalition’s took government and presented their first budget in 2014–15. During this time, 33,400 more people became unemployed, but government total spending to assist unemployed people has basically stayed the same. So government spending is going up significantly, there are more unemployed people, but individually they are receiving less support.

For how much saving? Over the next four years the $632 million is equivalent to 0.03% of total government estimated spending over that time. Why make life harder for 750,000 unemployed Australians for such a tiny saving?

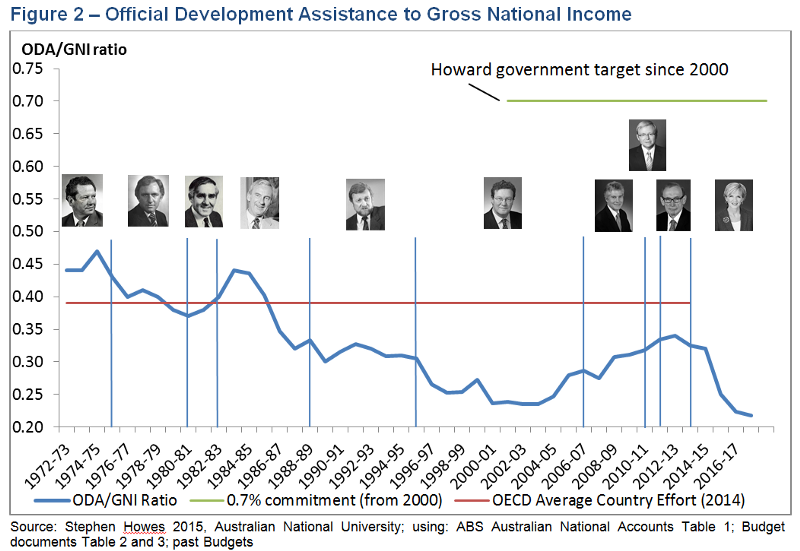

Shortsighted foreign aid cuts a broken Coalition promise

By Bill Browne, Researcher

Since the Howard Government, we’ve had bipartisan support that foreign aid spending should rise to 0.7% of Gross National Income. In other words, of every $100 of output, we should devote 70 cents to foreign aid.

It’s a reasonable target. The United Kingdom, Turkey, the United Arab Emirates and five other countries managed it last year.

Australia has been a little slower, but by the 2013 budget we’d set 2017 as the year when we were going to reach 0.5%. It’s no 0.7%, but it’s well above the OECD average of 0.32%.

In 2014 the aid budget was slashed, but Foreign Minister Julie Bishop assured us that it would “stabilise” at $5.3 billion in 2017.

So how much did foreign aid get in yesterday’s budget?

$3.4 billion, almost $2 billion below the “stabilisation” rate and even further below the around $7 billion that we would need to reach 0.5% of GNI … remembering that even that rate makes us a laggard compared to the UK, Turkey and the UAE!

In 2015, we declared Julie Bishop the “stingiest foreign minister” when foreign aid dropped more during her term than it did in any other foreign minister’s time in office. This budget will lock that title in.

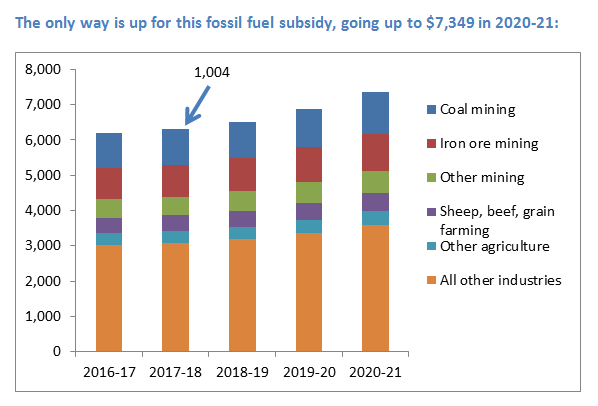

Congratulations Coal. You’ve hit $1 billion dollars — in subsidies

By Rod Campbell, Director of Research

If you drove your car to work on budget day, you paid tax on the fuel. If you’re a mining company, however, you generally don’t pay tax on your fuel. This is called the Fuel Tax Credits Scheme, and it cost taxpayers $6,194 million in 2016–17.

This graph breaks down the fuel subsidy by industry based on ATO tax statistics. The biggest beneficiary is the coal mining industry and 2017–18 is a big year — the tax break for coal will hit $1 billion for the first time! Congratulations coal industry!! Iron ore mining will have to wait until 2020–21 to hit the billion.

The coal industry will need that billion dollar hand out because the government seems to be hoping that the industry will pay for the development of “clean” coal. Spending on Resources and Energy is set to decrease by nearly 60% by 2020–21 because of:

a number of terminating measures, including the cessation of the Low Emissions Technology Demonstration Fund and Coal Mining Abatement Technology Support Package in 2016–17, and the cessation of funding for the … Carbon Capture and Storage Flagships programs in 2018–19.

While taxpayers are giving up on clean coal and planning to buy Snowy Hydro, renewable spending falters. Funding peaks this year at $357 million, declining to $214 million in 2020–21:

The overall decrease in expenses under the renewable energy component from 2017–18 to 2020–21 reflects the decrease in grants expenses for the Australian Renewable Energy Agency, which is partly offset by an increase in expenditure for the Clean Energy Finance Corporation.

Funny Money — How ScoMo Changed the Rules

By Dave Richardson, Senior Research Fellow

“Nothing is real; And nothing to get hung about”

In the lead up to the budget we heard a lot about ‘good and bad debt’. ‘Good debt’ is supposed to be that spent on capital investment such as infrastructure while ‘bad debt’ is that spent on recurrent. The split of course is nonsense. When you look at a $50 note there is no way you can tell what it was first spent on. Likewise when we look at a government security — what was it borrowed for? Welcome to the Byzantine world of government accounting.

[Editor’s note: The following is like a black diamond run of economics commentary. Continue at your own risk.]

Quick history: We have always had the normal cash accounts which gives the balance as just the sum of cash in minus cash out. Governments exploited that with asset sales, so those had to be excluded. Now the cash accounts give us the ‘underlying cash balance’ (excluding things like asset sales) and the ‘headline cash balance’ which is like the old normal cash accounts.

Still with me?

Some years ago the Howard government introduced accrual accounts. So we now have along side the cash accounts the accrual accounts modelled on commercial accounting principles. That gives the ‘operating balance’ similar to a company’s profit and loss statement and the ‘fiscal balance’ which is a new made-up concept to give the balance after adding capital investment to the operating balance.

This wasn’t complicated enough for ScoMo, so he has introduced a new concept of ‘recurrent spending’ and ‘capital spending’ and the ‘adjusted net operating balance’.

Capital spending totals $50.6 billion in 2017–18 made up of direct investment ($13.5 billion), capital grants to the states ($14.2 b) and ‘financial asset investments (policy purposes)’ ($22.9 b). If you took away the capital spending for 2017–18 you would eliminate the deficit now. But shucks the government is far too modest and deducts only $12.6 billion from the net operating balance. How that particular amount is derived is not explained.

So what?

A serious consequence of all this concerns investments in NBN Co, the new rail funding and so on. The budget papers announce a number of injections into a new government-owned company, WSA Co, to fund the Western Sydney Airport, and existing companies such as Australian Rail Track corporation for the Melbourne to Brisbane rail. These are included in ‘financial asset investments for policy purposes’ and are virtually treated as off budget.

As asset purchases they are excluded from the underlying balance but appear in the headline balance. So unless the government decides to brag about these investments they tend to take place without much mention in the budget papers. The budget papers mention them but give no details. Since these amount to $22.2 billion in 2017–18 there really should be more detail about what is a significant expenditure.

Incidentally — the budget papers now allocate debt among the spending departments. So Social Services is supposed to be responsible for debt of $233 billion or 48 per cent of all debt. Just for interest given the salary of the present Treasurer we think Mr Morrison is responsible for debt of $363,000.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

PM delays gas export tax | Between the Lines

The Wrap with Ebony Bennett Every week Australia delays introducing a 25% gas export tax is costing us $350 million. It’s a lot of lost revenue to ignore when your government has announced it will cut 160,000 people from the NDIS ahead of the federal budget. Yet, when the Prime Minister visited Perth this week, he seemed to kick the can down the road

Are we being lied to about what our nation can actually afford?

Did you notice what was different, really different, about the budget this year?

A moment to celebrate | Between the Lines

The Wrap with Greg Jericho It is easy for progressives to find things to complain about. It’s not because we are miserable, but unfortunately, we are too aware of the realities of life for many who never get a voice, aware of the crisis of climate change, and aware of the inequalities in the system