The latest wages price index figures show that for the first time since 2013 wages grew by more than 3% in the past year.

This growth is very welcome. It highlights that far from wages driving inflation, wage growth is only now beginning to grow at a pace that would be expected given the low level of unemployment. But as Labour Market and Fiscal Policy Director, Greg Jericho notes in his Guardian Australia column, while the level of wage growth we are seeing remains well below what would have been expected in the past with a 3.5% unemployment rate.

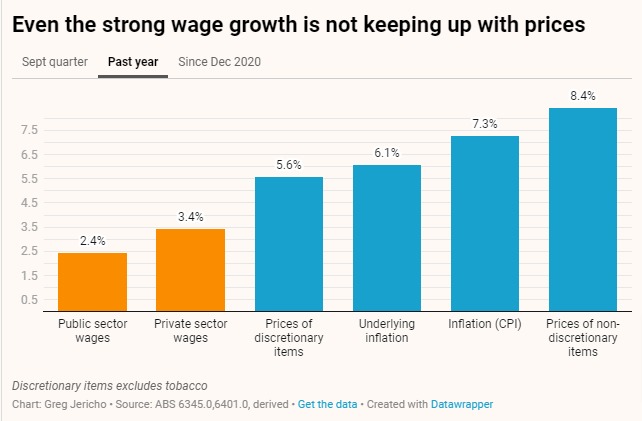

The strong growth came mostly from the private sector through a combination of new financial year individual contracts and the 5.2% minimum wage increase.

But even this is not enough to prevent real wages from falling for the 9th straight quarter. For more than 2 years now prices have been rising faster the wages. It has seen real wages fall back to 2011 levels after a 4.6% fall since September 2020.

The figures show that greater bargaining power is required for workers as they continue to lose out. The fastest wage growth for a decade should not see the biggest fall in real wages on record.

We know that greater enterprise bargaining producers better wages growth. That business groups are so against the provision in the Fair Work Amendment Bill demonstrates how worried they are about the ability of workers to have increased ability to bargain.

Profits have been growing faster than inflation, but wages are not.

The latest wage growth figures are pleasing to see, but they also demonstrate the challenges ahead, and just how greatly workers’ living standards have been hit by price rises that they did nothing to cause.

Between the Lines Newsletter

The biggest stories and the best analysis from the team at the Australia Institute, delivered to your inbox every fortnight.

You might also like

The Wage Price Index shows pay packets are up. So why doesn’t it feel that way?

The latest figures from the Australian Bureau of Statistics show wages are growing at a reasonable rate, but a deeper look shows a big problem might be about to bite Australian workers.

Delayed RBA cut is welcome, but borrowers are still lagging

The RBA has cut interest rates – five weeks too late.

“Vital” wage rise would be a lifeline to low income earners and wouldn’t drive inflation – new analysis

Updated analysis by The Australia Institute reveals that a fair and appropriate increase to the minimum wage, and accompanying increases to award rates, would not have a significant effect on inflation.